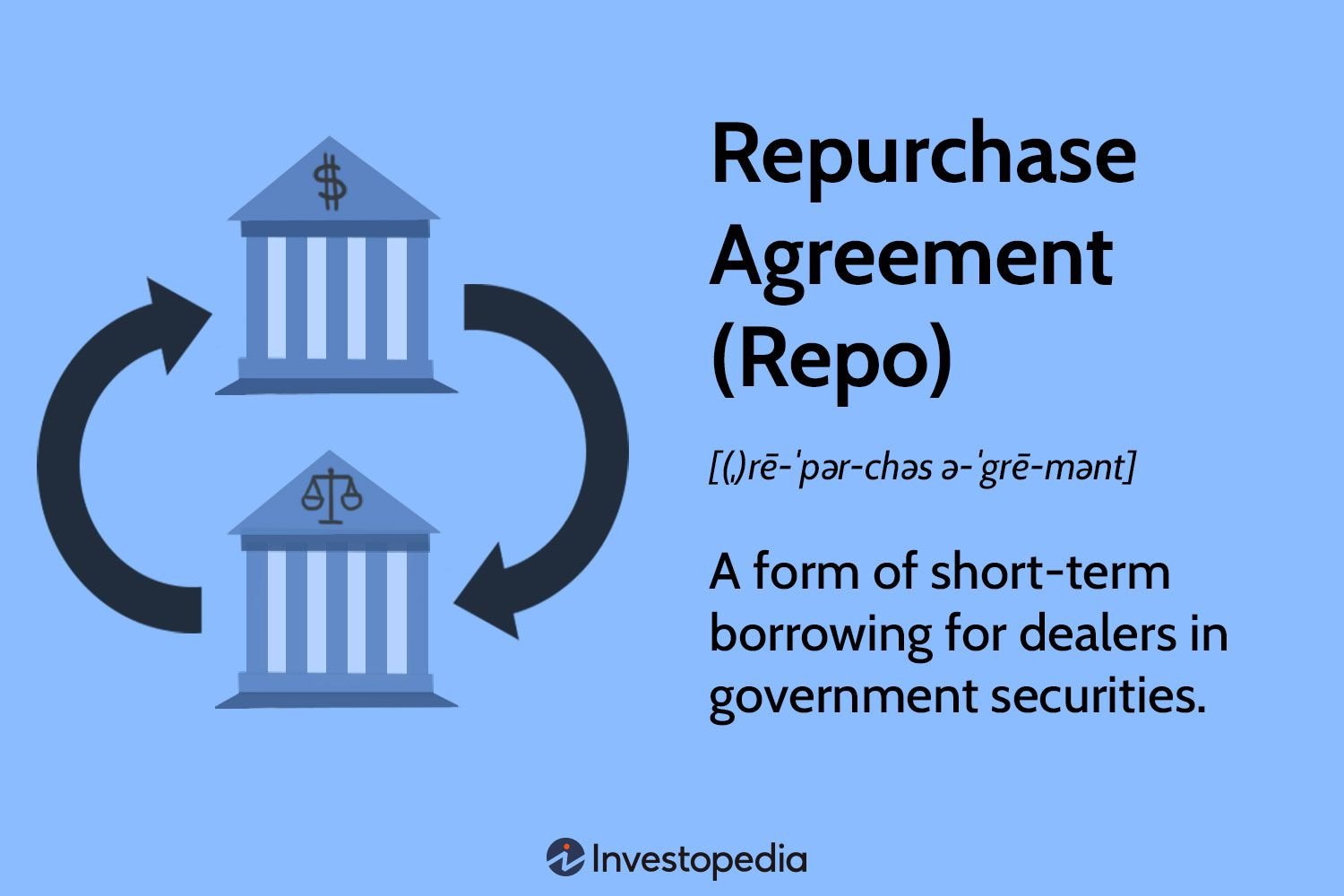

A repurchase agreement, also known as a repo, is a commonly used financial tool in the world of finance. Simply put, it is a short-term borrowing arrangement between two parties, typically a borrower and a lender. In a repo, the borrower sells a security to the lender with a promise to buy it back at a later date, usually the next day or within a few days, at a slightly higher price. This transaction effectively provides liquidity to the borrower while also providing a source of short-term investment for the lender. But what exactly does a repurchase agreement entail and how does it work? Let’s dive deeper into the intricacies of this financial arrangement.

What is a Repurchase Agreement in Finance?

A repurchase agreement, often referred to as a repo, is a financial instrument commonly used in the money markets. It is a short-term borrowing arrangement between two parties, typically a borrower and a lender, in which the borrower sells a financial security to the lender with an agreement to repurchase it at a later date at a slightly higher price. In essence, it is a collateralized loan, where the security serves as collateral for the funds borrowed.

Repos play a crucial role in the functioning of financial markets, providing liquidity and allowing participants to manage their short-term funding needs. They are widely used by banks, money market funds, government entities, and other financial institutions to obtain short-term financing or to invest excess cash.

Key Players in a Repurchase Agreement

To understand the functioning of repurchase agreements, it’s essential to be familiar with the key players involved:

1. Borrower: The borrower is the party in need of short-term funds. This could be a bank, a money market fund, or a government entity.

2. Lender: The lender provides the funds in exchange for the collateral. Lenders are often institutional investors, such as other banks, money market funds, or central banks.

3. Collateral: The collateral represents the security or financial instrument that the borrower sells to the lender. It provides assurance to the lender that they can recover their investment if the borrower defaults on repayment.

4. Tri-Party Agent: In some cases, a tri-party agent is involved to facilitate the transaction. The tri-party agent serves as an intermediary, holding the collateral on behalf of the lender and ensuring the proper execution of the repurchase agreement.

How Repurchase Agreements Work

Let’s walk through an example to understand the mechanics of a repurchase agreement:

1. The borrower approaches the lender and agrees to sell a specific financial security for a specified period, usually overnight or for a few days. The borrower transfers the security to the lender, who holds it as collateral.

2. In return, the lender provides funds to the borrower, equivalent to a percentage (known as the haircut) of the market value of the security. The haircut acts as a cushion, protecting the lender against potential declines in the security’s value.

3. The borrower pays interest to the lender for the duration of the agreement. The interest rate, known as the repo rate, is agreed upon by both parties and is typically based on prevailing market rates and the perceived creditworthiness of the borrower.

4. At the end of the agreed-upon period, the borrower repurchases the security from the lender at a slightly higher price, known as the repurchase price. The difference between the repurchase price and the original sale price represents the interest earned by the lender.

5. If the borrower fails to repurchase the security, the lender can sell the collateral in the open market to recover the funds lent. This ability to liquidate the collateral quickly adds an additional layer of security for the lender.

The Benefits of Repurchase Agreements

Repurchase agreements offer several benefits to market participants:

1. Liquidity Management: Repurchase agreements provide a means for institutions to manage their short-term liquidity needs without resorting to other costlier alternatives, such as borrowing from the central bank or issuing debt.

2. Short-term Financing: Borrowers can access short-term financing through repos without having to sell off long-term assets or disrupt their investment strategies. This flexibility allows institutions to meet their funding requirements efficiently.

3. Collateralized Lending: Lenders in repo transactions benefit from the collateral securing their investment. If the borrower defaults, the lender can sell the collateral, minimizing the risk of loss.

4. Interest Income: Lenders earn interest income through repo transactions, which can be an attractive investment option in a low-interest-rate environment.

5. Market Liquidity: The widespread use of repos in financial markets contributes to market liquidity as it allows participants to easily access short-term funding or invest their excess cash.

Variations of Repurchase Agreements

While the basic structure of repurchase agreements remains the same, there are variations that cater to specific needs and market conditions. Some notable variations include:

1. Open Repos: In an open repo, the term of the agreement is not fixed, and the borrower and lender can continue the arrangement until either party decides to terminate it. Open repos allow for greater flexibility.

2. Reverse Repos: In a reverse repo, the roles of the borrower and lender are reversed. The lender sells a security to the borrower with an agreement to repurchase it at a later date. Reverse repos are commonly used by central banks to absorb excess liquidity from the market.

3. Term Repos: Unlike overnight repos, term repos have a fixed term that extends beyond one day. They are usually utilized when parties require financing for an extended period.

4. Tri-Party Repos: In tri-party repos, a third-party agent acts as an intermediary between the borrower and the lender. The agent provides administrative services and custodial functions, streamlining the execution of the transaction.

The Risks Associated with Repurchase Agreements

While repurchase agreements offer various benefits, it’s important to be aware of the risks involved:

1. Counterparty Risk: The borrower may default on their obligation to repurchase the security, leading to potential losses for the lender. Conducting due diligence on the counterparty’s creditworthiness is crucial to mitigate this risk.

2. Market Risk: The value of the collateral can fluctuate during the term of the repo. If the value declines significantly, it may expose the lender to potential losses, even considering the haircut.

3. Operational Risk: The operational aspects of repo transactions, including the transfer of collateral and the settlement process, can introduce risks if not executed correctly. Proper documentation, clear legal agreements, and reliable custodial services are essential to mitigate operational risks.

Repurchase agreements are a fundamental component of the money markets, providing short-term liquidity and financing options for various institutions. They offer flexibility, security through collateralization, and a means to earn interest income. However, market participants should be aware of the risks associated with these transactions, including counterparty risk, market risk, and operational risk. With proper risk management and due diligence, repurchase agreements can be valuable tools for participants in the financial markets.

Repurchase Agreements (Repo) & Reverse Repurchase Agreements (Reverse Repo) Explained in One Minute

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What is a repurchase agreement in finance?

A repurchase agreement, also known as a repo, is a short-term financial transaction where one party (usually a borrower) sells securities to another party (usually a lender) with an agreement to repurchase them at a higher price in the future.

How does a repurchase agreement work?

In a repurchase agreement, the borrower sells securities to the lender and simultaneously agrees to buy them back at a predetermined price and date. This allows the borrower to obtain short-term funds while using the securities as collateral.

What types of securities are involved in repurchase agreements?

Commonly, Treasury bills, government bonds, and other highly liquid securities are used in repurchase agreements. These securities serve as collateral to secure the borrowed funds.

Who typically engages in repurchase agreements?

Financial institutions such as banks, broker-dealers, and hedge funds commonly engage in repurchase agreements. These transactions provide a way for them to manage their short-term cash needs or invest excess funds.

What are the benefits of repurchase agreements?

Repurchase agreements offer several benefits, including short-term liquidity, reduced credit risk due to the collateralization of the transaction, and potentially higher yields for lenders compared to other short-term investments.

What is the difference between a repurchase agreement and a loan?

In a repurchase agreement, securities are sold with an agreement to repurchase them, while in a loan, money is borrowed with an agreement to repay it. Repurchase agreements involve the use of collateral, whereas loans may or may not require collateral.

Are repurchase agreements considered safe investments?

Repurchase agreements are generally considered safe investments due to the use of collateral. However, like any investment, there is still some level of risk involved. It is important to assess the creditworthiness of the counterparty and understand the terms of the agreement.

Can individuals participate in repurchase agreements?

Although predominantly used by financial institutions, some individuals can participate in repurchase agreements through money market funds or other investment products. However, it is important for individuals to understand the associated risks before investing.

How are repurchase agreement transactions regulated?

Repurchase agreements are subject to regulation by financial authorities, such as central banks and securities regulators. These regulations aim to ensure transparency, stability, and fair practices in the repurchase agreement market.

Final Thoughts

A repurchase agreement, also known as a repo, is a financial transaction where one party sells securities to another party with an agreement to repurchase them at a later date. These agreements are commonly used in short-term borrowing and lending between financial institutions. The party selling the securities receives immediate cash while the party buying the securities earns interest on the investment. Repurchase agreements provide liquidity to the market and serve as an important tool for managing short-term funding needs. In finance, a repurchase agreement is a widely utilized mechanism for short-term financing and facilitating liquidity in the market.