Understanding interest rates in savings accounts is a crucial aspect of managing your finances wisely. If you’ve ever wondered how these rates are determined and what impact they have on your savings, you’ve come to the right place. In this article, we will delve into the intricacies of interest rates in savings accounts, providing you with the knowledge and tools necessary to make informed decisions about your money. So, whether you’re a seasoned saver or just starting out on your financial journey, join us as we navigate the world of interest rates and take control of your financial future.

Understanding Interest Rates in Savings Accounts

When it comes to saving money, one of the most important factors to consider is the interest rate offered by a savings account. Interest rates determine how much your savings will grow over time, making them a crucial aspect of financial planning. In this article, we will delve into the world of interest rates in savings accounts, discussing their significance, how they work, and factors that can affect them. So let’s dive in and unravel the mysteries of interest rates in savings accounts.

What is an Interest Rate in a Savings Account?

An interest rate is essentially the cost of borrowing money or the return on an investment. In the context of savings accounts, the interest rate is the percentage of your account balance that you earn as interest over a specific period, typically on an annual basis. This interest is basically the reward you receive from the bank for keeping your money with them. As a saver, the higher the interest rate, the more your money will grow over time.

Why Are Interest Rates Important in Savings Accounts?

Interest rates play a critical role in savings accounts for several reasons:

1. Accelerated Growth: By earning interest on your savings, your money can grow faster than if it simply sits idle in your account. Over time, compound interest can exponentially increase your savings, allowing you to reach your financial goals sooner.

2. Preserving Purchasing Power: Over time, inflation erodes the purchasing power of your money. Higher interest rates can help combat inflation by ensuring your savings keep up with the rising cost of living.

3. Building Emergency Funds: Savings accounts with competitive interest rates can help you build a solid emergency fund. The interest earned can provide a safety net for unexpected expenses or financial emergencies.

4. Financial Security: Savings accounts with higher interest rates can provide greater financial security, ensuring a stable return on your money. This can be especially beneficial in times of economic uncertainty.

How Do Interest Rates Work in Savings Accounts?

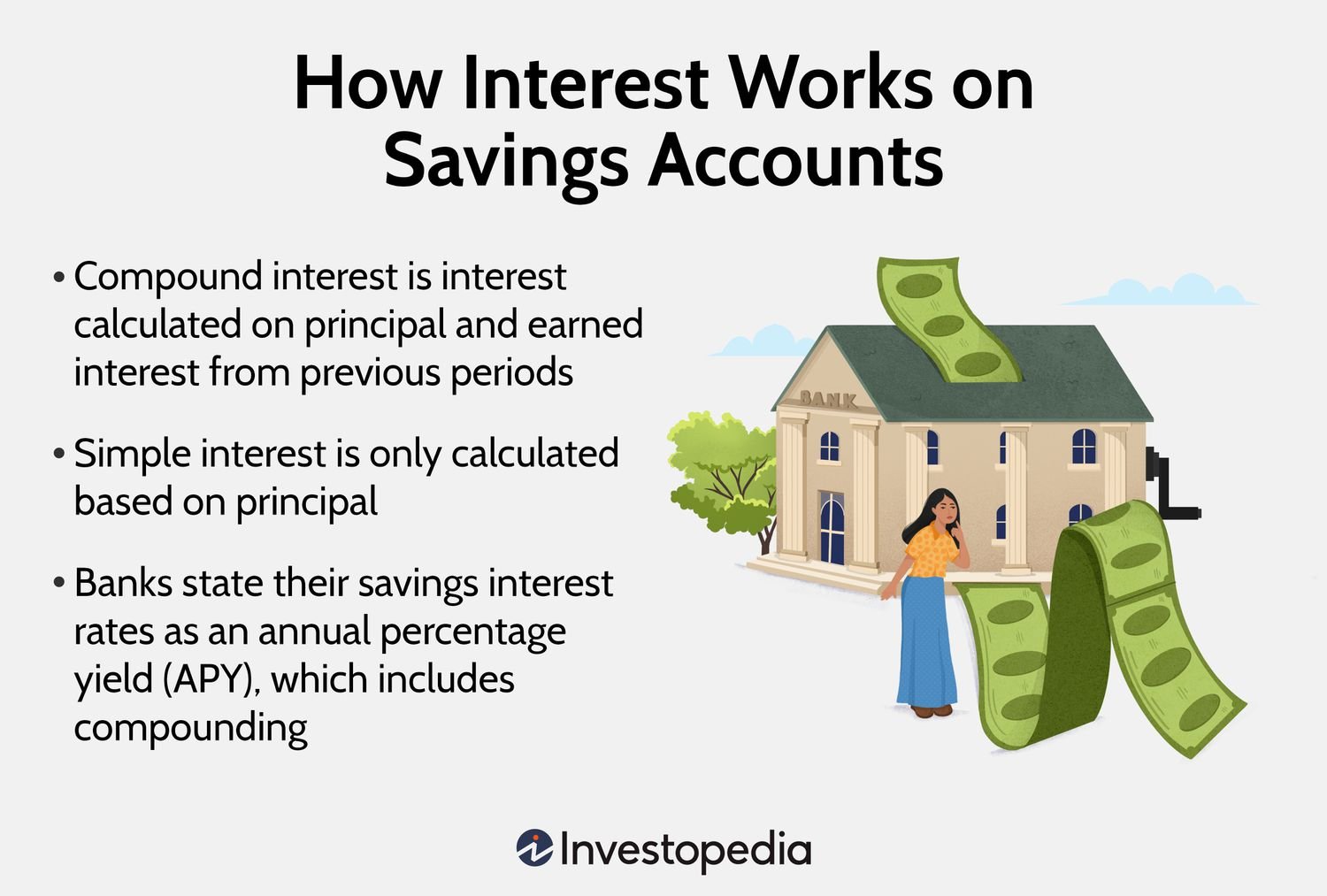

Interest rates in savings accounts are typically expressed as Annual Percentage Yield (APY). APY takes into account the compounding effect, which means that your interest earns more interest over time.

Here’s an example to illustrate how interest rates work in savings accounts:

Let’s say you have $10,000 in a savings account with a 2% APY. At the end of the first year, you would earn $200 in interest ($10,000 x 0.02). This would bring your total balance to $10,200. In the second year, your interest would be calculated based on this new balance, resulting in a slightly higher return. Over time, the compounding effect can significantly impact your savings.

Factors Affecting Interest Rates in Savings Accounts

Several factors can influence the interest rates offered by savings accounts. It’s essential to understand these factors to make informed decisions about where to save your money. Here are some key considerations:

1. Economic Conditions: Interest rates are influenced by broader economic conditions, including inflation, monetary policy, and market trends. When the economy is strong, interest rates tend to be higher, while they may be lower during periods of economic downturn.

2. Bank Policies: Each bank sets its own interest rates based on its financial strategies and goals. Some banks may offer higher rates to attract more customers, while others may focus on differentiating themselves in other ways.

3. Account Balance: Some banks offer tiered interest rates based on the amount of money you have in the account. Larger account balances may qualify for higher interest rates, incentivizing savers to consolidate their savings in one place.

4. Introductory Offers: Banks often provide promotional interest rates to attract new customers. These rates may be higher initially but could decrease after a specific period. It’s important to be aware of the terms and conditions to avoid any surprises later on.

Types of Savings Accounts

Now that we have a good understanding of interest rates in savings accounts, it’s worth considering the different types of savings accounts available. Each type has its own features and benefits, which can affect the interest rates offered. Let’s explore some common types of savings accounts:

1. Regular Savings Accounts

Regular savings accounts are the most basic and widely available type of savings account. They typically offer lower interest rates compared to other types of accounts. These accounts are ideal for individuals who want easy access to their funds and don’t have specific savings goals or requirements.

2. High-Yield Savings Accounts

High-yield savings accounts are designed to offer higher interest rates than regular savings accounts. These accounts may require a higher minimum balance or have certain limitations, such as a limited number of withdrawals per month. High-yield savings accounts are suitable for individuals who want to maximize their savings and are willing to meet the account requirements.

3. Money Market Accounts

Money market accounts are another type of savings account that typically offers competitive interest rates. These accounts may come with additional features, such as check-writing capabilities and debit card access. Money market accounts are ideal for individuals who want higher interest rates and some flexibility in accessing their funds.

4. Certificate of Deposit (CD)

A Certificate of Deposit (CD) is a time deposit that offers a fixed interest rate for a specific period, known as the term. CDs usually have higher interest rates than regular savings accounts but require locking your money for the duration of the term. They are suitable for individuals who don’t need immediate access to their funds and want to earn a higher interest rate.

Comparing Interest Rates in Savings Accounts

When comparing different savings accounts, it’s important to consider not only the interest rates but also other features and factors. Here are some key points to keep in mind:

- Check the APY: The Annual Percentage Yield (APY) takes compounding into account, giving you a more accurate picture of your potential earnings.

- Consider Minimum Balance Requirements: Some accounts may require a minimum balance to earn the advertised interest rate. Make sure you can maintain the required balance to avoid any penalties or reductions in interest rates.

- Fee Structure: Review the account’s fee structure, including monthly maintenance fees, transaction fees, and penalties. These fees can eat into your savings and lower your overall return.

- Accessibility: Determine how easily you can access your funds. Some accounts may have restrictions on withdrawals or require a waiting period.

- Customer Service: Take into account the quality of customer service provided by the bank. Accessibility to knowledgeable representatives can be crucial if you have any questions or concerns about your account.

Understanding interest rates in savings accounts is essential for effective financial planning. By considering the factors that influence interest rates and choosing the right type of savings account, you can optimize your savings growth. Remember to compare different options, weigh the features and benefits, and make an informed decision based on your financial goals. With the right savings account and a competitive interest rate, you can watch your money grow steadily over time and secure your financial future.

How Does Savings Account Interest Work?

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What are interest rates in savings accounts?

Interest rates in savings accounts refer to the percentage of money a bank or financial institution pays you for keeping your money in a savings account. It is essentially the cost of borrowing money from you, and the interest is usually calculated on an annual basis.

How do interest rates in savings accounts work?

Banks and financial institutions use interest rates to encourage individuals to save money. The interest you earn on your savings account is a portion of the money you have deposited, and it is paid to you on a regular basis. The higher the interest rate, the more money you can earn on your savings.

What factors determine the interest rates in savings accounts?

Several factors influence the interest rates in savings accounts, including the current economic conditions, the monetary policy set by the central bank, demand for loans, and the bank’s own financial condition. Banks also consider the amount of money you have in your account when determining the interest rate.

Do all banks offer the same interest rates in savings accounts?

No, different banks and financial institutions offer different interest rates on savings accounts. The rates can vary based on the bank’s policies, competition in the market, and the type of savings account you have. It is recommended to compare rates from different banks before choosing a savings account.

How are interest rates in savings accounts calculated?

Interest rates in savings accounts are typically calculated using two methods: simple interest and compound interest. Simple interest is calculated only on the principal amount, while compound interest takes into account the interest earned over previous periods as well.

Are interest rates in savings accounts fixed or variable?

Interest rates in savings accounts can be both fixed and variable. Fixed interest rates remain the same throughout the specified period, while variable interest rates can change over time based on market conditions. It is essential to check whether the interest rate on your savings account is fixed or variable.

Can interest rates in savings accounts change over time?

Yes, interest rates in savings accounts can change over time. Banks can adjust their rates to reflect changes in market conditions, monetary policies, or their own financial situation. These changes can be either an increase or a decrease in the interest rate, depending on the circumstances.

What are the benefits of higher interest rates in savings accounts?

Higher interest rates in savings accounts allow you to earn more money on your savings. They can help your savings grow faster and provide you with more financial security. Additionally, higher interest rates can potentially offset the impact of inflation, ensuring your money retains its value over time.

Final Thoughts

Understanding interest rates in savings accounts is crucial for anyone looking to grow their savings over time. When considering a savings account, it is important to compare interest rates offered by different banks and financial institutions. By doing so, individuals can make informed decisions about where to deposit their money. Additionally, understanding the concept of compound interest is essential to maximizing savings. The higher the interest rate and the more frequently it compounds, the faster savings will grow. So, take the time to research and compare interest rates in savings accounts to make the most of your hard-earned money.