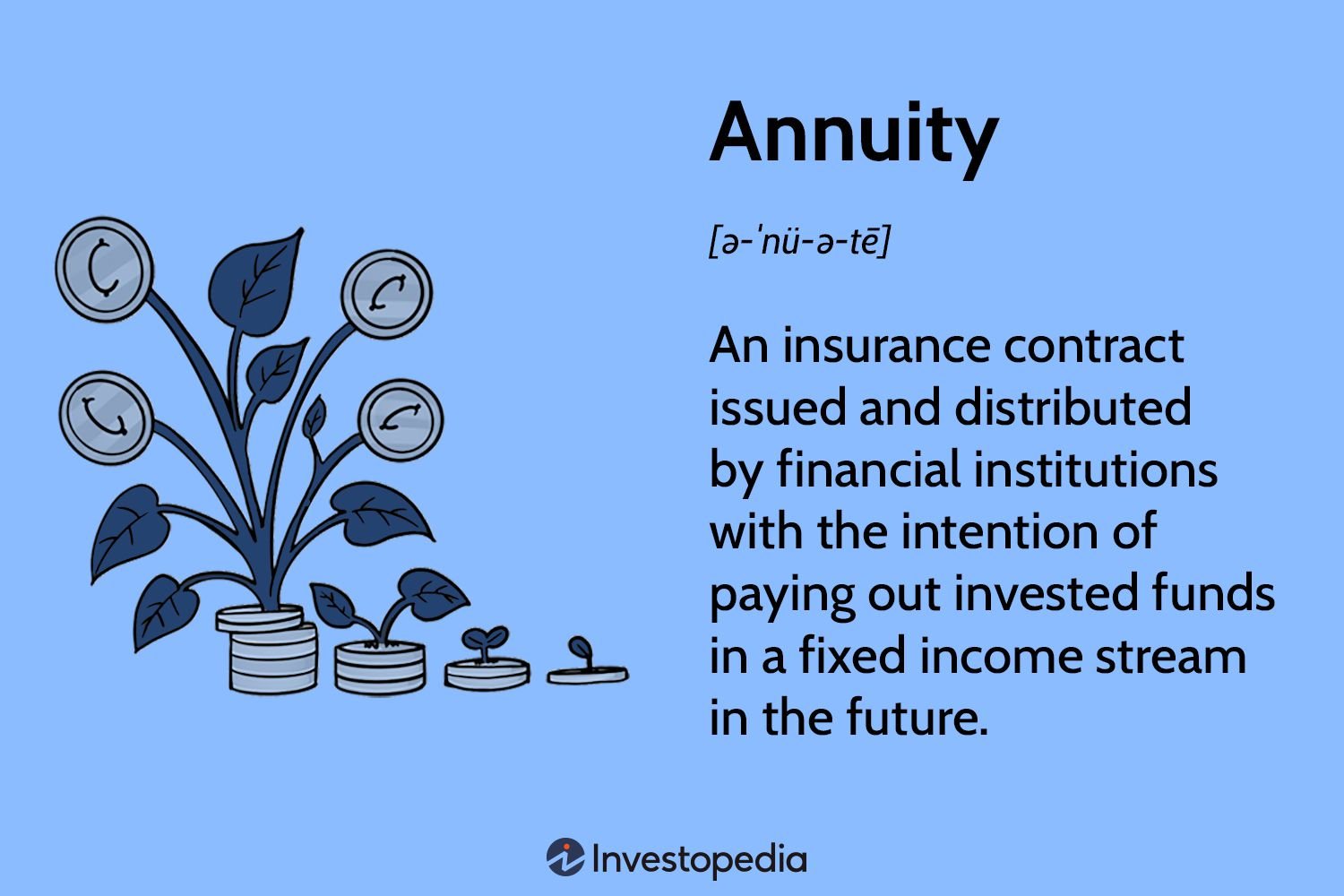

Have you ever wondered what annuities are and how they work? If you have, look no further! Annuities are financial products that provide a steady stream of income during retirement. They can be a valuable tool to help you achieve financial security in your later years. But how do they actually work? In this blog article, we will explore the ins and outs of annuities and demystify their inner workings. So, let’s dive right in and unravel the mystery of what annuities are and how they can benefit you on your journey to retirement.

What Are Annuities and How Do They Work?

Annuities are financial products that offer individuals a way to save and invest for retirement or receive a guaranteed income stream. They can be a valuable tool for long-term financial planning and ensuring a steady source of income during retirement. In this article, we will dive into the world of annuities, exploring what they are, how they work, and the various types available.

Understanding Annuities

An annuity is essentially a contract between an individual and an insurance company. In exchange for a lump sum payment or a series of payments, the insurance company promises to provide regular payments back to the individual at a future date or over a specific period of time. This regular income stream can be structured to last for a predetermined number of years or for the rest of the individual’s life.

Annuities are commonly used as retirement savings vehicles, as they provide a way for individuals to accumulate funds over time and then convert those funds into a steady income stream during retirement. They offer a level of financial security and stability, ensuring a consistent flow of income regardless of market fluctuations.

The Working Mechanism of Annuities

To understand how annuities work, it is important to familiarize yourself with some key concepts:

Accumulation Phase

During the accumulation phase, individuals contribute money to an annuity contract either through a lump sum payment or through periodic payments called premiums. The money grows on a tax-deferred basis, meaning it is not subject to taxes until it is withdrawn. This allows for potential compounding growth over time.

Guaranteed Interest Rate

Annuities often offer a guaranteed minimum interest rate. This means that even if the market performs poorly, the account value will still increase by the predetermined rate. However, it’s important to note that this rate is generally lower compared to other investment options.

Investment Options

Insurance companies provide individuals with different investment options for their annuity funds. These options may include fixed interest rate annuities, variable annuities, or indexed annuities.

– Fixed Rate Annuities: With fixed rate annuities, the interest rate is set at the time of purchase and remains unchanged throughout the accumulation phase. This provides stability and predictable returns.

– Variable Annuities: Variable annuities allow individuals to invest their funds in a variety of investment options such as stocks, bonds, and mutual funds. The returns are based on the performance of these underlying investments, meaning they can fluctuate with the market.

– Indexed Annuities: Indexed annuities combine elements of both fixed rate and variable annuities. The returns are linked to a specific index, such as the S&P 500. While the returns may be subject to a cap, indexed annuities offer the potential for higher returns based on the performance of the chosen index.

Beneficiary and Death Benefit

Annuities provide the option to designate a beneficiary. In the event of the annuity owner’s death, the beneficiary will receive the remaining value of the annuity. This can be structured as a lump sum payment or as continued regular payments.

Annuitization Phase

Once the individual reaches the designated retirement age, they can begin the annuitization phase. This involves converting the accumulated funds into regular income payments. The frequency and duration of these payments can be customized according to the individual’s needs and preferences.

Income Options

When it comes to receiving income from an annuity, individuals have several options:

– Lifetime Income: Individuals can choose to receive income for the rest of their lives. This provides a guaranteed stream of income, no matter how long they live.

– Period Certain Annuity: With a period certain annuity, individuals receive income for a specific period of time, such as 10, 15, or 20 years. If the annuitant passes away before the end of the period, the remaining payments may go to a beneficiary.

– Joint and Survivor Annuity: A joint and survivor annuity provides income for the individual and their spouse or partner for as long as either of them lives. This ensures that the surviving spouse continues to receive income after the annuitant’s death.

Tax Considerations

It’s important to understand the tax implications of annuities:

Tax-Deferred Growth

During the accumulation phase, annuities offer tax-deferred growth. This means that the funds can grow without being subject to annual taxes. However, when withdrawals or distributions are made, the earnings are taxed as ordinary income.

Early Withdrawal Penalties

If individuals withdraw funds from an annuity before the age of 59½, they may be subject to early withdrawal penalties. These penalties are similar to those imposed on early withdrawals from retirement accounts such as 401(k)s or IRAs.

Required Minimum Distributions

Once individuals reach the age of 72, they are generally required to take minimum distributions from their annuity accounts. This ensures that the funds are gradually distributed and taxed as income.

Types of Annuities

There are several types of annuities available to meet different financial goals and preferences:

Immediate Annuities

As the name implies, immediate annuities provide an immediate income stream. Individuals make a lump-sum payment to the insurance company, and in return, they start receiving regular payments immediately. Immediate annuities are suitable for those who want to convert their savings into a guaranteed income source without any delay.

Fixed Annuities

Fixed annuities offer a fixed interest rate for a specific period of time. The interest rate remains the same during the accumulation phase, providing stability and predictability for individuals who prefer a steady income stream.

Variable Annuities

Variable annuities allow individuals to invest their annuity funds in a range of investment options such as stocks, bonds, and mutual funds. The returns are variable and depend on the performance of the underlying investments.

Indexed Annuities

Indexed annuities provide returns that are linked to the performance of a specific index, such as the S&P 500. They offer the potential for higher returns while also providing a level of protection against market downturns.

Deferred Annuities

Deferred annuities have two phases: the accumulation phase and the annuitization phase. During the accumulation phase, individuals contribute premiums and let their funds grow over time. The annuitization phase begins at retirement when individuals convert their accumulated funds into regular income payments.

Choosing the Right Annuity

When selecting an annuity, it’s important to consider your financial goals, risk tolerance, and time horizon. Here are some key factors to keep in mind:

– Determine your retirement income needs: Assess your expenses and financial obligations during retirement to estimate the income you will require.

– Understand the fees and charges: Annuities often come with fees, such as administrative fees, mortality and expense charges, and investment management fees. Understand these costs and evaluate their impact on your overall returns.

– Seek professional advice: Consider consulting with a financial advisor who specializes in retirement planning and annuities. They can help you navigate the complexities of annuity products and guide you towards the most suitable choice for your needs.

Annuities can play a crucial role in retirement planning, providing individuals with a guaranteed income stream and financial security. By understanding how annuities work, the different types available, and the associated tax considerations, individuals can make informed decisions about incorporating annuities into their retirement strategy. Remember, everyone’s financial situation is unique, so it’s important to carefully evaluate your needs and consult with a financial professional before making any significant financial decisions.

What Is An Annuity And How Does It Work?

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What are annuities?

Annuities are financial products that provide a steady stream of income over a specified period of time, typically during retirement. They are usually purchased from insurance companies and can serve as a long-term investment vehicle to supplement other retirement savings.

How do annuities work?

Annuities work by individuals making an initial investment, either through a lump sum payment or periodic contributions. The insurance company then invests the funds and guarantees a series of payments to the annuity holder, typically starting at retirement age. The payments can be received in fixed amounts, variable amounts tied to market performance, or a combination of both.

Are there different types of annuities?

Yes, there are different types of annuities available. The main types are fixed annuities, variable annuities, and indexed annuities. Fixed annuities offer a guaranteed rate of return, while variable annuities involve investment in multiple funds, subject to market fluctuations. Indexed annuities offer a return based on a specific market index.

Can annuities help with retirement planning?

Yes, annuities can play an important role in retirement planning. They provide a reliable source of income that can be used to cover living expenses during retirement. Annuities can be used to complement other retirement savings, such as 401(k) plans and IRAs, and provide a steady stream of income throughout retirement.

What are the benefits of annuities?

One of the key benefits of annuities is the ability to receive a guaranteed income stream for a specified period or even for life. They can also offer tax advantages, such as tax-deferred growth and the option to receive income that is partially tax-free. Additionally, annuities provide a level of financial security and can protect against outliving your savings.

What are the drawbacks of annuities?

While annuities have their advantages, there are also some drawbacks to consider. Annuities often come with fees and expenses, which can reduce the overall return on investment. Additionally, annuities are inflexible, as the funds are typically locked in for a set period and early withdrawals may incur penalties. It’s essential to carefully review the terms and conditions before investing in an annuity.

Can annuities be inherited?

Yes, annuities can be inherited. If the annuity holder passes away, the funds can be passed on to a designated beneficiary. The beneficiary can choose to receive the remaining payments or take a lump sum payout, depending on the specific terms of the annuity contract and applicable tax laws.

Can annuities be cashed out early?

In most cases, annuities have surrender periods during which early withdrawals may result in penalties. However, some annuities have provisions that allow for penalty-free withdrawals under certain circumstances, such as terminal illness or long-term care needs. It’s important to review the terms of the annuity contract to understand the options and potential penalties for early withdrawal.

Final Thoughts

Annuities are financial products that provide a steady income stream in exchange for a lump sum or regular payments. They can be a useful tool for retirement planning and ensuring a reliable source of income. Annuities work by pooling funds from multiple individuals, which are then invested by the insurance company. The earnings from these investments are distributed to annuity holders in the form of regular payments. These payments can be fixed or variable, depending on the type of annuity chosen. Overall, annuities offer financial security and stability in retirement, making them an attractive option for many individuals.