Congratulations on your new addition to the family! As you embrace the joy and wonder of parenthood, it’s crucial to address the practical aspects too, such as financial planning. Don’t worry, we’ve got you covered with this comprehensive guide to financial planning for new parents. From budgeting for the future to safeguarding your child’s education, we’ll navigate through the complexities so you can make informed decisions. Let’s dive in and ensure a secure and stable financial future for your growing family.

Guide to Financial Planning for New Parents

Welcoming a new addition to the family is an exciting and joyous time for any couple. Along with all the love and happiness, parenthood also brings a wave of responsibilities, including the need for financial planning. As new parents, it is crucial to have a solid financial plan in place to ensure the well-being and future of your child. In this guide, we will walk you through the essential steps of financial planning for new parents, helping you navigate this new chapter with confidence.

The Importance of Financial Planning for New Parents

Becoming a parent is a life-changing event that requires adjustments in various aspects of your life, including your finances. Financial planning is essential for new parents for several reasons:

1. Financial Security: Adequate financial planning provides a safety net for your growing family, ensuring that you can meet your child’s needs and provide a stable home environment.

2. Education Expenses: Planning ahead can help you save for your child’s education, which is often a significant expense. By starting early, you can benefit from compounding interest and secure your child’s educational future.

3. Emergency Preparedness: Sudden financial emergencies can occur at any time. Creating an emergency fund is crucial to handle unexpected expenses, such as medical bills or home repairs.

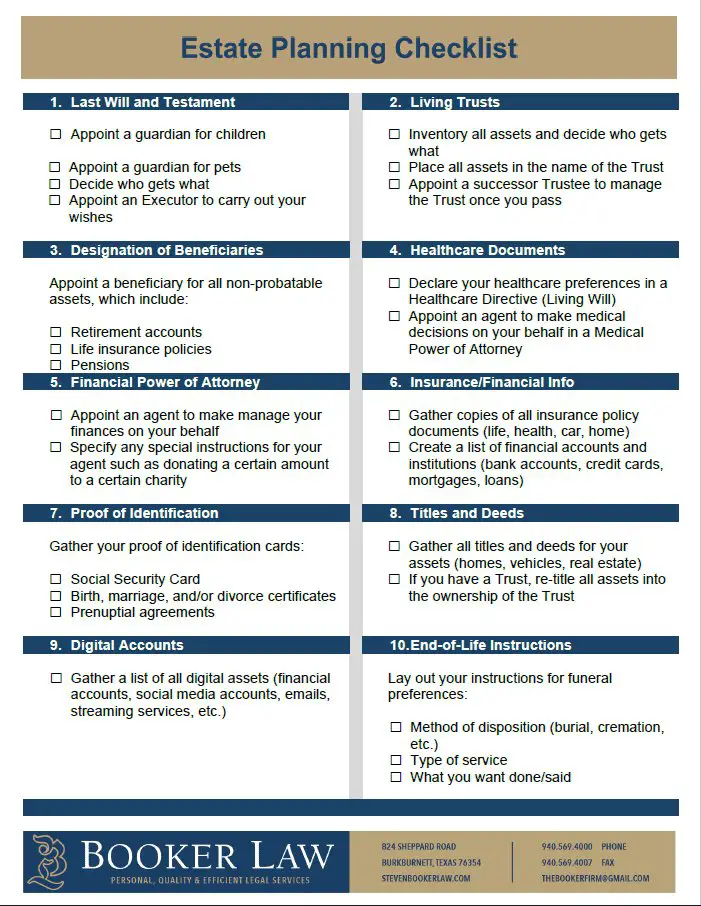

4. Protecting Your Child’s Future: Financial planning allows you to secure your child’s future by having adequate life insurance coverage and setting up a will or trust.

Assessing Your Current Financial Situation

Before diving into financial planning, it is vital to assess your current financial situation. Understanding your income, expenses, and savings will help you set realistic goals and make informed decisions. Here are some steps to get you started:

1. Calculate Your Income and Expenses: Begin by calculating your household income, including salaries, bonuses, and any other sources of revenue. Next, track your monthly expenses to determine where your money is going. Categorize your expenses into essential (such as food, housing, and transportation) and discretionary (like entertainment and dining out).

2. Review Your Debts: Take stock of your existing debts, such as student loans, credit card balances, and mortgages. Make a plan to pay off high-interest debts first to reduce financial stress in the long run.

3. Evaluate Your Saving and Investment Accounts: Assess your current savings and investment portfolio. Determine if you have an emergency fund and review your retirement savings. Consider opening a college savings account, such as a 529 plan, to start saving for your child’s education.

4. Check Your Insurance Coverage: Review your insurance policies, including health, life, and disability insurance. Ensure that you have adequate coverage for your family’s needs, taking into account potential medical expenses and income protection in case of unforeseen circumstances.

Setting Financial Goals

Once you have a clear picture of your current financial situation, it’s time to set goals for your family’s future. Goal setting helps you stay focused and motivated during your financial planning journey. Here are some common financial goals for new parents:

1. Create an Emergency Fund: Aim to save three to six months’ worth of living expenses in an easily accessible emergency fund. This helps protect your family in case of unexpected job loss, medical emergencies, or home repairs.

2. Save for Your Child’s Education: Determine how much you would like to contribute to your child’s education fund. Research the estimated costs of college education and set a target amount. Start saving early to take advantage of compound interest and various college savings plans.

3. Pay Off Debt: Develop a plan to pay off high-interest debts, such as credit cards and student loans. Prioritize your debts and create a budget that allows for accelerated debt repayment.

4. Save for Retirement: It’s never too early to think about retirement. Contribute regularly to your retirement savings accounts, such as employer-sponsored 401(k) plans or IRAs. Take advantage of any employer matching contributions.

Creating a Budget

A well-planned budget is the foundation of effective financial planning. It helps you monitor your income and expenses, ensuring that you can meet your financial goals. Here’s how to create a budget as new parents:

1. List Your Income and Expenses: Start by listing your monthly income sources. Then, categorize your expenses into fixed (e.g., mortgage, insurance premiums) and variable (e.g., groceries, entertainment). Don’t forget to include savings as an expense category.

2. Set Realistic Spending Targets: Analyze your expenses and identify areas where you can cut back or save money. Consider your financial goals when setting spending targets for different expense categories.

3. Track and Adjust: Keep track of your expenses and monitor your budget regularly. Use budgeting apps or spreadsheets to simplify the process. Adjust your budget as needed to align with your financial goals and changing circumstances.

Insurance and Estate Planning

As new parents, it is crucial to protect your family’s well-being through appropriate insurance and estate planning. Here are some essential steps to consider:

1. Life Insurance: Invest in life insurance to financially secure your family’s future in the event of your untimely passing. Evaluate your coverage needs based on your income, outstanding debts, and future expenses, such as your child’s education.

2. Health Insurance: Ensure that you and your family have comprehensive health insurance coverage. Research different plans to find the one that suits your needs best.

3. Disability Insurance: Protect your income by considering disability insurance. This coverage provides financial support if you are unable to work due to a disability or illness.

4. Create a Will or Trust: Consult with an attorney to establish a will or trust. This ensures that your assets are distributed according to your wishes and that a guardian is appointed for your child if something were to happen to both parents.

5. Appoint Beneficiaries: Review and update beneficiaries on your life insurance policies, retirement accounts, and other financial assets to ensure they align with your current wishes.

Investing for the Future

Investing is a crucial part of financial planning, helping you grow your wealth over time. Consider these investment strategies as new parents:

1. Start Early: Take advantage of compounding interest by starting to invest as soon as possible. The earlier you start, the more time your investments have to grow.

2. Invest According to Risk Tolerance: Determine your risk tolerance and choose investments accordingly. While stocks offer higher potential returns, they also come with more significant risks. Consider diversifying your portfolio with a mix of stocks, bonds, and other assets.

3. Consider College Savings Plans: Explore college savings plans, such as 529 plans, which offer tax advantages when saving for your child’s education. Research different options to find the best fit for your family.

4. Consult a Financial Advisor: If you feel overwhelmed or unsure about investment strategies, seek guidance from a qualified financial advisor. They can provide personalized advice based on your unique circumstances.

Regularly Review and Adjust Your Financial Plan

Financial planning is not a one-time task; it requires regular review and adjustments. As your family grows and circumstances change, revisit your financial plan at least once a year or whenever a significant life event occurs. Consider the following:

1. Monitor Your Progress: Keep track of how you’re progressing toward your financial goals. Regularly review your budget, savings, investments, and insurance coverage.

2. Adjust for Life Changes: Update your financial plan to accommodate changes such as a new job, salary increase, or a new addition to the family. Make sure your plan reflects your current circumstances.

3. Revisit Your Goals: Periodically reassess your financial goals to ensure they align with your long-term vision. Adjust your goals if necessary and reallocate your resources accordingly.

4. Stay Informed: Stay updated on financial news and trends that may impact your investments or insurance coverage. Seek professional advice whenever needed to make informed decisions.

Financial planning is a crucial aspect of successfully navigating the journey of parenthood. By assessing your current financial situation, setting goals, creating a budget, protecting your family through insurance and estate planning, and investing wisely, you can build a solid foundation for your child’s future. Remember to regularly review and adjust your financial plan to ensure it aligns with your changing circumstances. With a well-thought-out financial plan in place, you can focus on enjoying the precious moments of parenthood while securing a bright future for your family.

Financial Planning Tips For New Parents

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What is financial planning for new parents?

Financial planning for new parents refers to the process of managing and organizing your finances to meet the needs of your growing family. It involves setting financial goals, creating a budget, saving for future expenses, and ensuring the financial security of your children.

Why is financial planning important for new parents?

Financial planning is crucial for new parents as it helps them prepare for the future and make informed decisions about their finances. It provides a roadmap to meet financial goals, builds a stable financial foundation, and ensures the well-being and security of their children.

How can I create a budget for my family?

To create a budget for your family, start by calculating your monthly income and listing all your expenses. Categorize your expenses into essential (such as housing, food, and healthcare) and discretionary (such as entertainment and dining out). Allocate a portion of your income towards savings and emergency funds. Regularly review and adjust your budget as needed.

What are some essential tips for saving money as new parents?

– Track your expenses and identify areas where you can cut back.

– Prioritize your spending and differentiate between wants and needs.

– Look for ways to save on everyday items such as diapers, baby clothes, and baby gear.

– Consider shopping for secondhand items and taking advantage of sales or discounts.

– Automate your savings by setting up automatic transfers to a savings account.

How can I plan for my child’s education expenses?

Planning for your child’s education expenses is essential. Start by estimating the future costs of education, taking into account inflation. Explore different education savings options, such as 529 plans or education savings accounts. Consistently contribute to these accounts and review your savings strategy periodically.

Is it necessary to have life insurance as new parents?

Having life insurance is highly recommended for new parents. It provides financial protection for your family in case of an untimely death. Life insurance can cover funeral expenses, outstanding debts, and ensure that your children’s future financial needs are met.

What are some ways to start saving for my child’s future?

– Open a dedicated savings account for your child’s future expenses.

– Contribute regularly to a college savings plan or a custodial account.

– Explore investment options such as mutual funds or index funds.

– Consider purchasing savings bonds or long-term investment plans.

– Consult with a financial planner to determine the best savings approach for your specific situation.

How can I ensure the financial security of my family in case of an emergency?

To ensure the financial security of your family in case of an emergency, it’s important to:

– Build an emergency fund that covers at least three to six months of expenses.

– Purchase adequate health insurance and consider supplementary coverage if needed.

– Review and update your estate planning documents such as wills and guardianship arrangements.

– Consider disability insurance coverage to protect against loss of income due to illness or injury.

– Regularly review and update your insurance policies to ensure they meet your family’s needs.

Final Thoughts

In conclusion, this guide provides new parents with valuable insights and actionable steps for effective financial planning. By prioritizing budgeting, emergency funds, insurance, and investments, parents can secure their financial future while providing for their growing family. Understanding the importance of expenses, setting realistic financial goals, and seeking professional advice when needed are key elements of successful financial planning. By following this guide to financial planning for new parents, they can ensure a stable and secure financial foundation for their children’s upbringing and future aspirations.