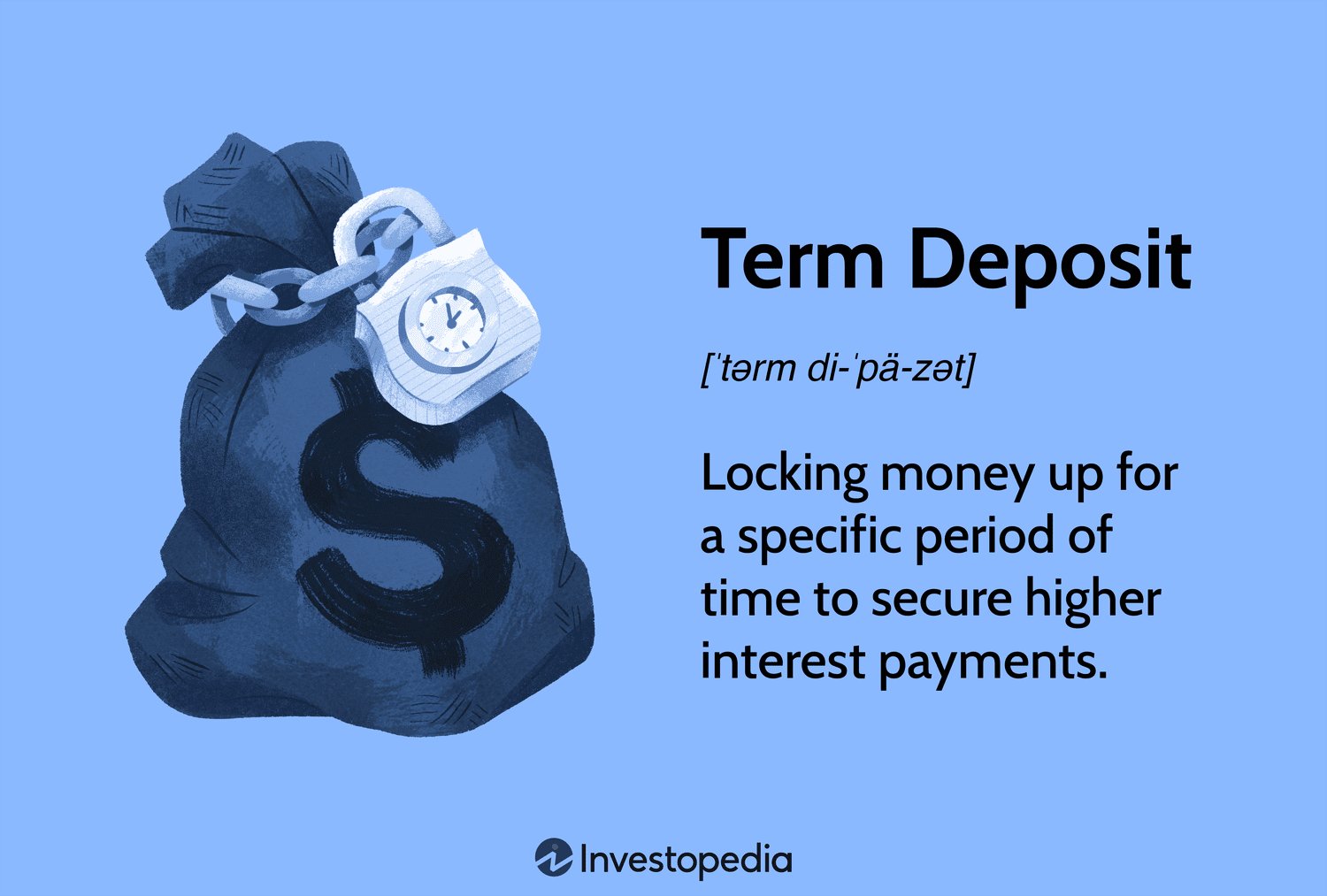

Looking to grow your savings while minimizing risk? Understanding the benefits of term deposits is the key. Term deposits offer a secure and straightforward way to earn interest on your money over a specific period of time. By investing in a term deposit, you can enjoy the peace of mind that comes with a fixed interest rate and a guaranteed return on your investment. In this article, we’ll delve into the advantages of term deposits and how they can help you achieve your financial goals. So, if you’re ready to explore the benefits of term deposits, let’s dive in!

Understanding the Benefits of Term Deposits

Term deposits are a popular investment option that can provide individuals with a secure and predictable way to grow their savings. In this article, we will explore the various benefits of term deposits, how they work, and why they may be a suitable choice for your financial goals. Whether you’re a first-time investor or someone looking to diversify their portfolio, understanding the advantages of term deposits can help you make informed decisions about your money.

1. Guaranteed Returns

One of the primary benefits of term deposits is that they offer guaranteed returns on your investment. When you deposit your money into a term deposit account, the bank or financial institution promises to pay you a fixed interest rate over a specified period of time. This means that regardless of fluctuations in the market, you can rest assured knowing exactly how much your investment will grow.

Unlike other investment options, such as stocks or mutual funds, term deposits are not subject to market volatility. This makes them an attractive choice for individuals who prefer a low-risk investment strategy or those who prioritize stability over potential high returns. With the assurance of guaranteed returns, term deposits can provide peace of mind and financial security.

2. Flexible Term Lengths

Term deposits offer flexibility in terms of the duration of your investment. The term length can typically range from a few months to several years, allowing you to choose a timeframe that aligns with your financial goals. Whether you’re saving for a short-term expense or a long-term objective, you can select the appropriate term length to suit your needs.

Short-term term deposits are ideal for individuals who require access to their funds in the near future or want to take advantage of higher interest rates within a specific time frame. On the other hand, long-term term deposits are suitable for those who can afford to lock their money away for a more extended period and benefit from potentially higher interest rates.

3. Earnings and Interest Rates

When you invest in a term deposit, you earn interest on your principal amount. The interest rates for term deposits are typically higher than those offered on regular savings accounts. The exact rate may vary depending on the bank or financial institution, the term length, and prevailing market conditions.

Term deposit interest rates are usually fixed for the duration of the investment, meaning they don’t change over time. This allows you to accurately estimate your earnings and plan your finances accordingly. Additionally, since term deposits operate on a compound interest basis, your earnings can grow even further as interest is added to your initial investment.

3.1. Comparing Interest Rates

Before committing to a term deposit, it’s important to compare interest rates offered by different banks or financial institutions. By conducting thorough research, you can identify the institutions that provide the most competitive rates, helping you maximize your returns.

Consider utilizing online comparison tools or consulting with a financial advisor to ensure you make an informed decision. Remember that even a slight difference in interest rates can significantly impact your earnings over the term of your deposit.

4. Easy and Convenient

Investing in term deposits is typically a straightforward and hassle-free process. Most banks and financial institutions allow you to open an account and deposit your funds online or in-person. The application process is simple, requiring minimal paperwork and often no fees.

Once your term deposit is established, you don’t have to worry about actively managing your investment. Unlike stocks or other forms of investments that may require constant monitoring, term deposits are a set-and-forget option. This convenience is particularly appealing to individuals with a busy lifestyle or those who prefer a hands-off approach to their investments.

5. Capital Preservation

Term deposits are known for preserving capital, making them a low-risk investment. When you invest in a term deposit, your principal amount is protected from market fluctuations and remains intact. Regardless of any shifts in the economy, you are guaranteed to receive your initial investment back at the end of the term.

This makes term deposits an attractive option for individuals who prioritize capital preservation and want to minimize the risk of losing their hard-earned money. If you’re looking for an investment avenue that offers stability and security, term deposits can be an excellent choice.

6. Diversification Strategy

Diversification is an essential aspect of any investment strategy. By spreading your investments across different asset classes, you can reduce risk and potentially enhance returns. Term deposits can play a valuable role in diversifying your investment portfolio.

While term deposits may not offer the same level of returns as higher-risk investments, they provide stability and a guaranteed rate of return. By allocating a portion of your portfolio to term deposits, you can balance out the overall risk and potentially achieve a more consistent and predictable stream of income.

7. Suitable for Retirement Planning

Term deposits can be particularly advantageous for retirement planning. As individuals approach their golden years, they often seek investment options that offer stability, predictable returns, and capital preservation. Term deposits can fulfill these requirements.

By incorporating term deposits into your retirement savings strategy, you can secure a portion of your funds and ensure a steady income stream during your retirement years. The fixed interest rates and guaranteed returns make term deposits an attractive option for retirees who rely on their savings to cover living expenses.

8. Early Withdrawal Options

While term deposits are designed to be held until maturity, unexpected circumstances may arise requiring you to access your funds before the term ends. Many financial institutions offer early withdrawal options, although they may come with certain conditions and penalties.

Before opening a term deposit account, it’s essential to inquire about the terms and conditions surrounding early withdrawals. Understanding the penalties or limitations associated with accessing your funds prematurely can help you make an informed decision and avoid any potential financial consequences.

It’s important to note that early withdrawals may result in a reduction of your overall returns, as the interest accrued may be adjusted or forfeited. Therefore, if you anticipate needing immediate access to your funds, it may be wise to explore alternative investment options that offer more flexibility.

9. Taxation Considerations

When investing in term deposits, it’s important to consider the taxation implications. The interest earned on term deposits is generally subject to income tax. The specific tax rate may vary depending on your country of residence and applicable tax laws.

Before investing, consult with a tax advisor who can provide guidance on the tax implications of term deposits in your specific jurisdiction. Understanding the potential tax liabilities can help you accurately estimate your overall returns and ensure compliance with relevant tax regulations.

10. Factors to Consider

While term deposits offer numerous benefits, it’s essential to consider the following factors before making a decision:

- Interest Rate: Compare interest rates offered by different institutions to maximize your returns.

- Term Length: Choose a term length that aligns with your financial goals and liquidity needs.

- Penalties: Familiarize yourself with any penalties or fees associated with early withdrawals.

- Taxation: Understand the tax implications of term deposits and consult with a tax advisor.

- Financial Goals: Assess whether term deposits align with your short-term and long-term financial objectives.

By considering these factors and conducting thorough research, you can make an informed decision that suits your financial circumstances and goals.

What are term deposits?

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What are the benefits of term deposits?

Term deposits offer several benefits, including:

How do term deposits work?

Term deposits involve depositing a specific amount of money with a financial institution for a fixed period of time, known as the term. During this term, the money earns interest at a predetermined rate. At the end of the term, the initial deposit plus the interest is returned to the depositor.

What is the typical term length for a term deposit?

The term length for a term deposit can vary, typically ranging from a few months to several years. It is important to choose a term length that aligns with your financial goals and needs.

Are term deposits FDIC insured?

In the United States, term deposits offered by FDIC-insured financial institutions are generally insured up to $250,000 per depositor. It’s essential to check with your specific financial institution to ensure your deposits are covered by FDIC insurance.

Can I withdraw money from a term deposit before the end of the term?

In most cases, withdrawing money from a term deposit before the end of the term is subject to penalties. These penalties may include a reduction in interest earned or a fee charged by the financial institution. It’s advisable to carefully consider your financial needs before committing to a term deposit.

What happens when a term deposit matures?

When a term deposit reaches its maturity date, the financial institution will notify you. You will then have the option to withdraw the funds or reinvest them in a new term deposit. If you choose not to take any action, the financial institution may automatically renew the term deposit for the same term length.

Can I add funds to a term deposit?

In general, once a term deposit is established, additional funds cannot be added until the deposit matures. However, you can open a new term deposit with the additional funds separately.

How are interest rates determined for term deposits?

Interest rates for term deposits are determined by various factors, including prevailing market rates, the length of the term, and the financial institution’s policies. It’s advisable to compare rates from different institutions to find the most competitive option that suits your needs.

Final Thoughts

Understanding the benefits of term deposits is crucial for making informed financial decisions. Term deposits offer a secure way to grow your savings with guaranteed returns over a fixed period. They provide stability and protection against market fluctuations, making them a reliable investment option. By locking in your money for a specific term, you can enjoy higher interest rates and potentially maximize your earnings. Furthermore, term deposits offer flexibility with various maturity options, enabling you to align your investment goals with your financial timeline. In summary, term deposits are a beneficial financial tool that offers security, stability, and potential growth for your savings.