Understanding the wash-sale rule in stock trading can be a key factor in maximizing your investment strategy. But what exactly is this rule, and how does it affect your trades? In simple terms, the wash-sale rule is a regulation enforced by the Internal Revenue Service (IRS) that prevents investors from claiming a tax deduction on a stock sale if a similar stock is repurchased within a short period of time. It’s important to grasp the implications of this rule, as it can impact your profits and tax obligations. So, let’s delve into the nitty-gritty of the wash-sale rule and shed light on its implications for your stock trades.

Understanding the Wash-Sale Rule in Stock Trading

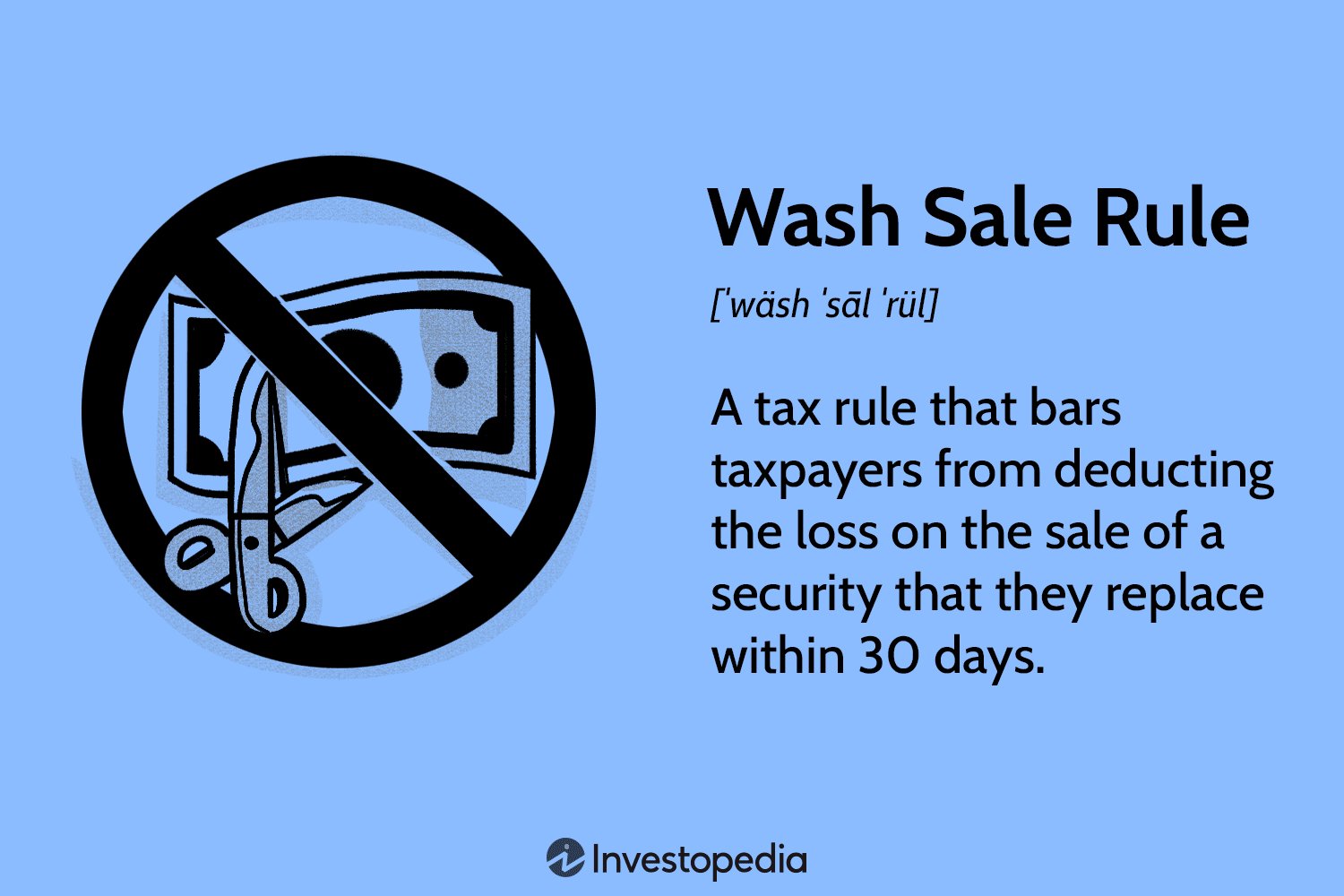

What is the Wash-Sale Rule?

The wash-sale rule in stock trading is an important regulation that governs the buying and selling of stocks for individual investors. It was established by the Internal Revenue Service (IRS) to prevent taxpayers from claiming artificial losses by selling stocks at a loss and repurchasing them shortly after. This rule ensures that investors cannot manipulate their taxable income by engaging in certain types of transactions.

According to the wash-sale rule, if you sell a stock at a loss and repurchase a substantially identical stock within 30 days before or after the sale, you cannot claim the loss for tax purposes. Instead, the loss is disallowed, and the cost basis of the repurchased stock is adjusted to include the disallowed loss. This rule aims to discourage investors from engaging in tax-driven artificial transactions while still allowing for legitimate investment strategies.

Why was the Wash-Sale Rule Implemented?

The primary reason behind implementing the wash-sale rule is to ensure fairness and prevent tax abuse. Without this rule, investors could potentially manipulate their taxable income by intentionally selling stocks at a loss to offset gains from other investments. By repurchasing the stock immediately after, they could effectively capture the tax benefits of the loss while maintaining their original investment position.

The wash-sale rule acts as a deterrent against these artificial transactions, maintaining the integrity of the tax system and preventing the loss of government revenue. It ensures that taxpayers pay the appropriate amount of tax by disallowing losses that are not truly realized from genuine investment activities.

How Does the Wash-Sale Rule Work?

To better understand the wash-sale rule, let’s take a closer look at its mechanics and how it affects stock trading:

1. Selling a Stock at a Loss: The first step in triggering the wash-sale rule is selling a stock at a loss. This loss can be used to offset any capital gains realized from other investments, thereby reducing your overall tax liability. However, if you plan to repurchase a substantially identical stock within 30 days, the wash-sale rule comes into play.

2. Repurchasing a Substantially Identical Stock: If you buy back the same stock within the 30-day window, the wash-sale rule is triggered, disallowing the loss you initially claimed. The disallowed loss is added to the cost basis of the newly acquired stock. This adjustment prevents you from claiming an artificial loss for tax purposes.

3. Impact on Tax Reporting: When preparing your tax return, you need to account for any wash-sale transactions properly. The IRS requires you to adjust the cost basis of the repurchased stock to include the disallowed loss. This adjustment affects the calculation of capital gains or losses when you eventually sell the repurchased shares.

4. Substantially Identical Securities: The wash-sale rule applies not only to the exact same stock but also to securities that are substantially identical. This includes stocks of the same company but with different ticker symbols, options contracts, or even shares of similar exchange-traded funds (ETFs). It’s crucial to understand what constitutes a substantially identical security to ensure compliance with the rule.

Exceptions to the Wash-Sale Rule

While the wash-sale rule generally disallows losses from certain transactions, there are some exceptions and scenarios where the rule does not apply:

1. Different Accounts: If you sell a stock in one investment account and repurchase it in another unrelated account, the wash-sale rule does not apply. The rule specifically applies to transactions occurring within the same account or accounts under common control.

2. Losses Before 30 Days: If you repurchase a stock before selling it at a loss within 30 days, the wash-sale rule does not come into effect. This means that purchasing a stock first and then selling it at a loss will not trigger the disallowance of the loss.

3. Stock Option Exercise: When exercising stock options, the wash-sale rule may not apply. However, specific rules and regulations govern the tax treatment of stock options, so it’s essential to consult a tax professional or refer to IRS guidelines.

4. IRA and Retirement Accounts: The wash-sale rule does not apply to transactions made within individual retirement accounts (IRAs) or other tax-advantaged retirement accounts. Any losses or gains within these accounts are generally not subject to immediate taxation or wash-sale restrictions.

It’s important to note that these exceptions have their own unique rules and considerations. Consulting with a tax advisor or professional is always recommended to ensure compliance with tax laws and regulations.

Implications and Strategies for Traders

Understanding the wash-sale rule is crucial for traders and investors to optimize their tax positions and avoid unintended consequences. Here are some implications and strategies to consider:

1. Tax Planning: Since the wash-sale rule disallows losses, it’s essential to plan your trades strategically to minimize its impact. By strategically timing your trades and understanding the 30-day window, you can optimize your tax positions and potentially defer losses to future tax years.

2. Record Keeping: Maintaining accurate records of your trades is essential for complying with the wash-sale rule. Keep detailed track of your purchase and sale dates, quantities, and prices. This documentation will help you accurately calculate your cost basis, disallowed losses, and potential future gains.

3. Harvesting Losses: Despite the wash-sale rule, you can still take advantage of tax loss harvesting strategies. By selling a stock at a loss and then purchasing a similar but not substantially identical stock, you can still realize losses for tax purposes while maintaining your investment exposure. This strategy allows you to offset gains and potentially lower your tax liability.

4. Adjusted Cost Basis Considerations: The wash-sale rule’s adjustment to the cost basis of repurchased stock affects future tax calculations. When eventually selling the repurchased stock, be aware that the disallowed loss will reduce your taxable gain or increase your deductible loss. Understanding these implications can help you plan and manage your tax liabilities effectively.

5. Seek Professional Guidance: The tax code is complex, and the wash-sale rule has several nuances and exceptions. If you actively trade or have complex investment strategies, consulting with a tax professional or accountant can provide valuable insights and ensure compliance with tax laws.

Understanding the wash-sale rule is vital for any investor or trader engaged in stock trading. Complying with the rule helps maintain the integrity of the tax system and ensures fairness for all taxpayers. By familiarizing yourself with the mechanics, exceptions, and strategies associated with the wash-sale rule, you can optimize your tax positions and make informed investment decisions. Remember to consult with a tax professional to navigate the complexities of the tax code and implement suitable strategies tailored to your individual circumstances.

The Wash Sale Rule

Frequently Asked Questions

Understanding the Wash-Sale Rule in Stock Trading

Frequently Asked Questions (FAQs)

What is the wash-sale rule in stock trading?

The wash-sale rule is a regulation by the Internal Revenue Service (IRS) that prevents investors from claiming tax deductions on the sale of a security if they repurchase a substantially identical security within a specific period.

How does the wash-sale rule work?

If an investor sells a stock or security at a loss and repurchases the same or a substantially identical security within 30 days before or after the sale, the wash-sale rule is triggered. The investor cannot claim a tax deduction for the loss during that tax year.

Can the wash-sale rule apply to both gains and losses?

No, the wash-sale rule only applies to losses. If an investor sells a security at a gain and repurchases the same or substantially identical security within the wash-sale period, there are no restrictions or limitations.

What is the wash-sale period?

The wash-sale period begins 30 days before the sale of the security and ends 30 days after the sale. Any repurchase of the same or substantially identical security during this period triggers the wash-sale rule.

Can the wash-sale rule apply to different types of securities?

Yes, the wash-sale rule applies not only to stocks but also to options, bonds, mutual funds, and other types of securities. The rule applies across various investments as long as they are considered substantially identical.

Can the wash-sale rule apply to different brokerage accounts?

Yes, the wash-sale rule applies to all brokerage accounts that an investor holds. It considers all accounts owned by the same taxpayer when determining if a wash sale has occurred.

What are the consequences of violating the wash-sale rule?

If an investor violates the wash-sale rule, the loss from the sale of the securities is disallowed for current tax purposes. Instead, the disallowed loss is added to the cost basis of the repurchased security, effectively deferring the loss until a future sale.

Are there any exceptions to the wash-sale rule?

There are no exceptions to the wash-sale rule. It applies to all investors, whether they are individuals, corporations, or other entities engaged in stock trading or investment activities.

How can investors avoid triggering the wash-sale rule?

Investors can avoid triggering the wash-sale rule by waiting for at least 31 days before repurchasing the same or substantially identical security after selling at a loss. This ensures that the sale is not considered a wash sale and allows for the deduction of the loss in the current tax year.

Final Thoughts

Understanding the wash-sale rule in stock trading is essential for investors to navigate the complexities of the market. This rule prevents investors from claiming tax losses on the sale of a security if a substantially identical security is repurchased within a certain timeframe. By avoiding wash sales, investors can optimize their tax strategies and ensure they comply with the regulations set forth by tax authorities. It is crucial for traders to be aware of this rule and seek professional advice to maximize their gains and minimize potential penalties. Understanding the wash-sale rule in stock trading is paramount for any investor looking to navigate the market successfully.