Inflation can be a worrisome concept for many investors. The steady erosion of purchasing power can eat away at the value of their investments over time. However, there is a solution: inflation-protected securities. These unique financial instruments provide a shield against the negative effects of inflation, ensuring that investors can maintain the purchasing power of their money. But what are inflation-protected securities exactly? In this article, we will delve into the world of these securities and explore how they can safeguard your portfolio in an inflationary environment. Get ready to understand the ins and outs of inflation-protected securities and make informed investment decisions. Let’s dive in!

What are Inflation-Protected Securities?

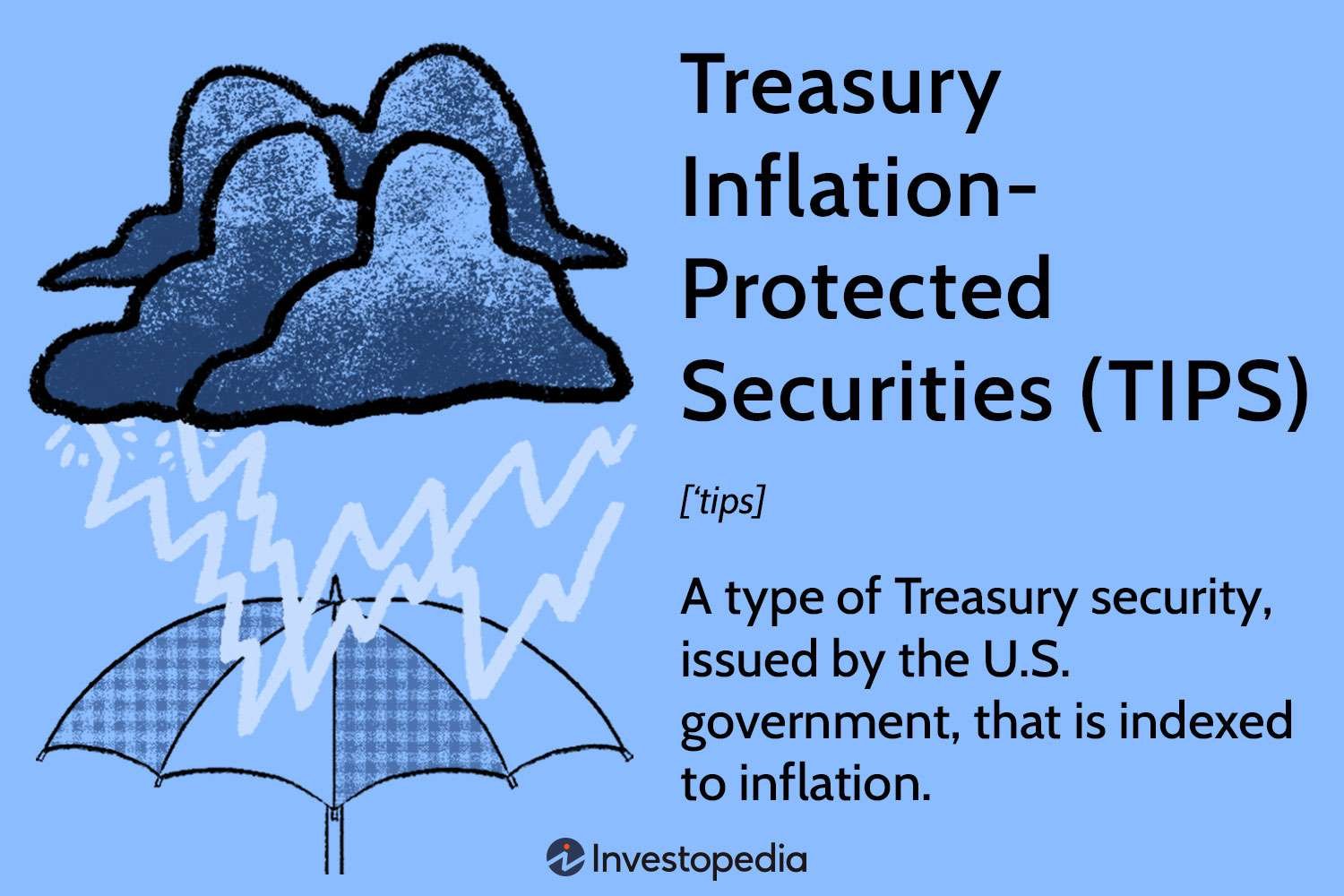

Inflation-protected securities, also known as Treasury inflation-protected securities (TIPS), are investment instruments issued by the U.S. Treasury to protect investors from the negative effects of inflation. These securities offer a reliable way to preserve the purchasing power of your money over time by adjusting their principal value based on changes in inflation.

TIPS were first introduced in 1997 and have gained popularity among both individual and institutional investors due to their unique characteristics. Unlike traditional fixed-income securities that pay a fixed interest rate, the principal value of TIPS adjusts with the Consumer Price Index (CPI), which measures changes in the cost of goods and services.

How Do Inflation-Protected Securities Work?

When you invest in TIPS, the principal amount you initially invest is adjusted according to the CPI. This means that if there is an increase in inflation, the principal value of your TIPS will rise, keeping pace with the rising prices of goods and services. Consequently, the interest payments you receive from TIPS also increase as the principal value grows.

The interest payments on TIPS are paid semiannually and are based on the adjusted principal value. The interest rate, also known as the coupon rate, is fixed and determined at the time of issuance. However, the actual amount of interest you receive may vary as it is calculated based on the adjusted principal value.

The Benefits of Inflation-Protected Securities

Investing in inflation-protected securities offers several advantages, making them an appealing option for investors looking to hedge against inflation and maintain the purchasing power of their investments. Some of the key benefits of TIPS include:

1. Protection against inflation: TIPS provide a built-in safeguard against inflation by adjusting the principal value in accordance with changes in the CPI. This ensures that your investment keeps pace with rising prices.

2. Predictable income: The interest payments on TIPS are fixed and paid semiannually. This provides investors with a predictable income stream, making it easier to plan and budget.

3. Preservation of purchasing power: By investing in TIPS, you can preserve the purchasing power of your money over time. The adjustments made to the principal value help offset the erosion of value caused by inflation.

4. Diversification: Including TIPS in your investment portfolio can add diversification benefits. TIPS tend to have a low correlation with other asset classes, such as stocks and traditional bonds, making them a valuable tool for risk management.

5. Tax advantages: The interest income received from TIPS is subject to federal income tax, but it is exempt from state and local taxes. This tax advantage can enhance the overall return on your investment.

Types of Inflation-Protected Securities

There are primarily two types of inflation-protected securities: Treasury Inflation-Protected Securities (TIPS) and Treasury Inflation-Protected Securities with a Constant Maturity (TIPS-CM).

1. Treasury Inflation-Protected Securities (TIPS): These are the most common type of inflation-protected securities. They are issued with maturities of 5, 10, and 30 years and are available for purchase directly from the U.S. Treasury or through a broker.

2. Treasury Inflation-Protected Securities with a Constant Maturity (TIPS-CM): TIPS-CM are a relatively new addition to the Treasury’s inflation-protected securities offerings. They have a fixed maturity of 10 years and are issued with regular reopenings to ensure a continuous supply in the market.

How to Buy Inflation-Protected Securities

Investing in inflation-protected securities can be done through various channels. Here are the most common ways to buy TIPS:

1. Directly from the U.S. Treasury: You can purchase TIPS directly from the U.S. Treasury through their online platform known as TreasuryDirect. This allows you to buy TIPS at auction and manage your investments directly.

2. Through a broker: Many brokerage firms offer access to a wide range of fixed-income securities, including TIPS. By opening an account with a broker, you can buy and sell TIPS in the secondary market.

3. Exchange-Traded Funds (ETFs): Another option to invest in TIPS is through ETFs that hold a diversified portfolio of inflation-protected securities. ETFs provide the advantage of easy tradability and can be bought or sold on major stock exchanges.

4. Mutual Funds: Mutual funds specializing in inflation-protected securities can also offer exposure to TIPS. These funds pool money from multiple investors and invest in a diversified portfolio of inflation-protected securities.

It’s important to consider your investment goals, risk tolerance, and time horizon before deciding on the most suitable method for purchasing TIPS.

Risks and Considerations

While inflation-protected securities offer compelling benefits, it’s crucial to be aware of the potential risks and considerations associated with investing in TIPS:

1. Interest rate risk: Inflation-protected securities, like other fixed-income investments, are affected by changes in interest rates. When interest rates rise, the value of existing TIPS may decline in the secondary market.

2. Market risk: The market value of TIPS can fluctuate due to supply and demand dynamics and changes in investor sentiment. These market fluctuations can impact the value of your investment, especially if you decide to sell before maturity.

3. Deflation risk: While TIPS protect against inflation, they do not provide the same level of protection in the event of deflation. If prices decline, the principal value of TIPS will decrease, which may lead to a lower return on investment.

4. Opportunity cost: TIPS typically offer lower yields compared to traditional fixed-income securities. While TIPS provide protection against inflation, investors should consider the potential opportunity cost of investing in lower-yielding securities.

5. Tax implications: While the interest income from TIPS is exempt from state and local taxes, it is subject to federal income tax. Consult a tax advisor to understand the tax implications specific to your situation.

6. Individual circumstances: Consider your individual circumstances, investment goals, and risk tolerance before investing in TIPS. It’s essential to align your investment strategy with your specific financial objectives.

Inflation-protected securities, such as Treasury inflation-protected securities (TIPS), are government-issued investment instruments that provide a hedge against inflation. By adjusting the principal value based on changes in the CPI, TIPS help investors preserve the purchasing power of their money over time.

TIPS offer several benefits, including protection against inflation, predictable income, preservation of purchasing power, diversification opportunities, and tax advantages. Investors can buy TIPS directly from the U.S. Treasury, through a broker, or invest in ETFs or mutual funds specializing in inflation-protected securities.

As with any investment, it’s important to consider the risks and potential drawbacks associated with investing in TIPS, such as interest rate risk, market risk, deflation risk, opportunity cost, tax implications, and individual circumstances. By understanding these factors, investors can make informed decisions about incorporating inflation-protected securities into their investment portfolios.

What are TIPS – Treasury Inflation Protected Securities

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What are inflation-protected securities?

Inflation-protected securities, also known as Treasury Inflation-Protected Securities (TIPS), are bonds issued by the U.S. Treasury that protect investors against inflation. These securities are designed to help preserve the purchasing power of the investor’s principal by adjusting the bond’s value in response to changes in inflation.

How do inflation-protected securities work?

Inflation-protected securities work by adjusting their principal value based on changes in the Consumer Price Index (CPI), which measures inflation. As the CPI rises, the principal value of the security increases, and as it falls, the principal value decreases. This adjustment is made semi-annually, ensuring that the security keeps pace with inflation.

Who issues inflation-protected securities?

Inflation-protected securities are issued by the U.S. Treasury Department. The Treasury issues TIPS with various maturities, ranging from 5 to 30 years, allowing investors to choose the investment horizon that suits their needs.

What are the benefits of investing in inflation-protected securities?

Investing in inflation-protected securities provides several benefits. Firstly, they offer protection against inflation, ensuring that the investor’s purchasing power is maintained. Secondly, they provide a predictable income stream, as the interest payments on TIPS are adjusted for inflation. Lastly, inflation-protected securities are backed by the full faith and credit of the U.S. government, making them a relatively safe investment.

Are inflation-protected securities suitable for all investors?

While inflation-protected securities can be beneficial for many investors, they may not be suitable for everyone. Investors who are concerned about inflation eroding the value of their investments and those seeking a reliable income stream may find TIPS attractive. However, investors with a shorter investment horizon or those looking for potentially higher returns may find other investment options more suitable.

How can I purchase inflation-protected securities?

Inflation-protected securities can be purchased directly from the U.S. Treasury through their website, TreasuryDirect.gov. Investors can open an account, choose the desired TIPS, and place an order. Alternatively, investors can also purchase TIPS through a broker.

What is the minimum investment required for inflation-protected securities?

The minimum investment required for inflation-protected securities depends on the specific TIPS being purchased. Currently, the minimum denomination for TIPS is $100.

Can inflation-protected securities be sold before maturity?

Yes, inflation-protected securities can be sold before maturity. Investors have the option to sell their TIPS on the secondary market. The price at which the security is sold may be higher or lower than the original purchase price, depending on prevailing market conditions.

Are inflation-protected securities taxable?

Yes, inflation-protected securities are taxable at the federal level. While the principal adjustment for inflation is not taxed until maturity, the interest payments received from TIPS are subject to federal income tax. However, they are exempt from state and local taxes. It is advisable to consult a tax advisor for specific tax implications based on individual circumstances.

Final Thoughts

Inflation-protected securities, also known as inflation-indexed bonds or TIPS, are investments that shield investors from the erosion of purchasing power caused by inflation. These securities provide a safe haven against rising prices by adjusting their value in line with inflation measures, such as the Consumer Price Index (CPI). By holding inflation-protected securities, investors can ensure that their returns keep pace with inflation, preventing a decline in real value. These securities offer a reliable inflation hedge and can be a valuable addition to a well-diversified investment portfolio. With inflation posing a constant threat to the value of money, considering inflation-protected securities is a prudent move for investors seeking stability and protection against the impact of rising prices.