Syndicated loans are a vital tool in the world of finance, allowing businesses to secure large sums of money for various purposes. These loans involve a group of lenders who come together to provide funds to a borrower. But what exactly are syndicated loans and how do they work? Well, the answer lies in understanding the concept of pooling resources. When a borrower needs a substantial loan, a syndicate of lenders is formed, each contributing a portion of the total amount. This collaborative approach spreads the risk and allows for greater flexibility in terms of loan size and repayment terms. Let’s delve deeper into the fascinating world of syndicated loans and explore how they function.

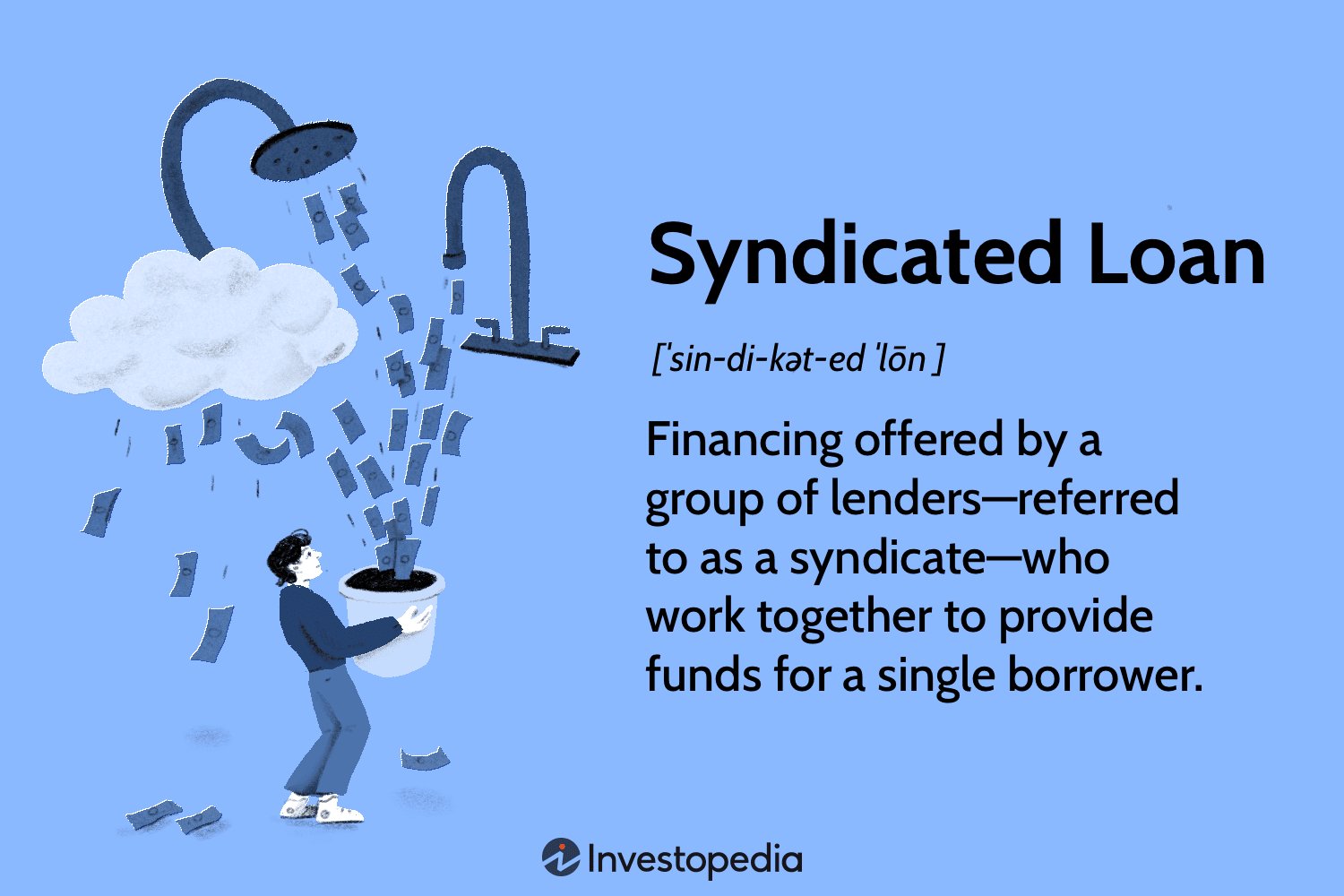

What Are Syndicated Loans and How Do They Work?

Syndicated loans are a form of financing that involves multiple lenders pooling their resources to provide a loan to a borrower. This type of loan is commonly used by large corporations, government entities, and other organizations that require substantial amounts of capital for various purposes. Syndicated loans offer several advantages, such as increased borrowing capacity, flexibility, and specialized expertise from participating lenders. In this article, we will delve deeper into the concept of syndicated loans, examining how they work and why they are a popular choice for borrowers in need of substantial funding.

1. Understanding Syndicated Loans

A syndicated loan involves a group of lenders, known as a syndicate, providing funds to a borrower. The borrower, typically a company or government entity, receives a single loan facility from the syndicate, while the risk and financial commitment are divided among the participating lenders. This structure enables lenders to spread their exposure to a single borrower and reduce their risk.

1.1 Primary Syndication vs. Secondary Syndication

Syndicated loans can be categorized into two stages: primary syndication and secondary syndication.

During the primary syndication stage, the lead arranger or underwriter, often a bank or financial institution with expertise in structuring large loans, is responsible for soliciting potential lenders to participate in the loan. These lenders could be commercial banks, institutional investors, or other financial entities. The lead arranger negotiates the terms of the loan on behalf of the borrower and coordinates the syndication process.

Once the loan agreement is finalized, the secondary syndication stage begins. At this point, the lead arranger distributes the loan among the participating lenders in predetermined portions, depending on their desired exposure and financial capacity. The lead arranger may retain a portion of the loan for its own account. This secondary syndication process allows lenders to buy and sell portions of the loan to other institutions, often through specialized loan-trading platforms.

2. How Does a Syndicated Loan Work?

To better understand how syndicated loans work, let’s explore the step-by-step process from the perspective of the borrower and the lenders:

2.1 Borrower’s Perspective

– Determine Borrowing Needs: The borrower assesses its funding requirements for a specific project, acquisition, or refinancing. The borrower identifies the amount of capital needed, the repayment terms, and the overall structure of the loan.

– Selecting a Lead Arranger: The borrower appoints a lead arranger, typically a financial institution with extensive experience in structuring and arranging syndicated loans. The lead arranger works closely with the borrower to define the loan structure, negotiate terms, and coordinate the syndication process.

– Underwriting and Documentation: The lead arranger, along with other participating lenders, conducts a thorough due diligence process to assess the creditworthiness and financial stability of the borrower. Once the due diligence is complete, the lead arranger prepares the necessary loan documentation, including the term sheet, loan agreement, and security agreements.

– Syndication Process: The lead arranger reaches out to potential lenders to participate in the syndicated loan. The lead arranger presents the loan opportunity, highlighting its key features and benefits. Interested lenders then submit indications of interest, stating their desired participation levels and pricing expectations.

– Allocation and Closing: Once the indications of interest are received, the lead arranger evaluates the lenders’ proposals and determines the final allocation of the loan among the participating lenders. The borrower and the lead arranger negotiate final loan terms and pricing. Upon agreement, the loan is closed, and the funds are disbursed to the borrower.

– Loan Administration: After the loan is disbursed, the lead arranger typically takes on the responsibility of administering the loan on behalf of the syndicate. This includes collecting interest and principal payments from the borrower and distributing them to the participating lenders. The lead arranger also handles any amendments, waivers, or other ongoing loan administrative tasks.

2.2 Lender’s Perspective

– Evaluating Loan Opportunities: Lenders assess potential syndicated loan opportunities based on the borrower’s creditworthiness, the purpose of the loan, and the overall market conditions. Lenders consider factors such as industry trends, economic outlook, and the borrower’s financial statements.

– Indication of Interest: Interested lenders submit indications of interest to the lead arranger, expressing their willingness to participate in the syndicated loan. Lenders specify the amount they are willing to lend, the pricing expectations, and any other terms they deem important.

– Due Diligence: If the lead arranger shortlists a lender based on their indication of interest, the lender conducts a thorough due diligence process to assess the borrower’s creditworthiness. This involves analyzing financial statements, reviewing business plans, and evaluating any collateral or guarantees offered by the borrower.

– Loan Allocation: The lead arranger evaluates all the indications of interest received and determines the final allocation of the loan among the participating lenders. The lead arranger considers factors such as the lenders’ desired participation levels, expertise in the borrower’s industry, and pricing expectations.

– Negotiating Terms: Once the loan allocation is determined, the lead arranger negotiates final terms and pricing with the borrower. Lenders may have the opportunity to provide input during this process, especially if they are taking on a significant portion of the loan.

– Loan Disbursement: Once the loan agreement is finalized, lenders disburse their allocated portion of the loan to the borrower through the lead arranger. The lead arranger handles all the disbursements and ensures the funds are transferred securely.

– Loan Administration: Lenders rely on the lead arranger to administer the loan on their behalf. The lead arranger manages ongoing loan administrative tasks, such as coordinating interest and principal payments, monitoring the borrower’s financial performance, and handling any amendments or waivers requested by the borrower.

3. Advantages and Benefits of Syndicated Loans

Syndicated loans offer several advantages to both borrowers and lenders. Let’s explore some of the key benefits:

3.1 Borrower’s Benefits

– Access to Large Amounts of Capital: Syndicated loans allow borrowers to raise substantial amounts of capital that may not be available through traditional bank financing or other debt instruments.

– Diversification of Lenders: By involving multiple lenders, borrowers can tap into a diverse network of financial institutions and investors, each with their own areas of expertise and risk appetite.

– Tailored Loan Structures: Syndicated loans offer flexibility in structuring loan terms, repayment schedules, and covenants. Borrowers can negotiate terms that align with their specific financial needs and goals.

– Efficient Execution: Syndicated loans are often quicker to arrange compared to other forms of financing. This can be advantageous for borrowers who require immediate access to funds for time-sensitive projects or acquisitions.

– Relationship Building: Engaging with multiple lenders through a syndicated loan can help borrowers establish long-term relationships with financial institutions and investors. These relationships can be valuable for future financing needs.

3.2 Lender’s Benefits

– Risk Mitigation: Syndicated loans enable lenders to distribute their exposure to a single borrower across multiple participants. This diversification reduces the risk associated with a default by the borrower.

– Enhanced Deal Flow: Lenders participating in syndicated loans gain access to a broader range of lending opportunities than they would individually. This increases the chances of finding attractive investment opportunities.

– Expertise Sharing: Participating lenders can leverage the specialized knowledge and industry expertise of other syndicate members. This collaboration helps lenders make informed lending decisions and mitigate risks.

– Flexible Investment Sizes: Syndicated loans offer lenders the flexibility to invest different amounts based on their risk appetite and available capital. Lenders can choose to participate in the loan at varying levels, allowing for greater investment diversification.

– Fee Income: Lenders involved in syndicated loans earn fees for underwriting and arranging the loan. These fees, often a percentage of the loan amount, contribute to the lender’s overall income.

4. Risks and Considerations of Syndicated Loans

While syndicated loans provide various advantages, it’s essential to be aware of the potential risks and considerations associated with this form of financing:

4.1 Borrower’s Risks

– Higher Costs: Syndicated loans may involve higher costs compared to traditional bank loans. This is because borrowers need to compensate the lead arranger and participating lenders through fees, commitment charges, and higher interest rates.

– Complex Loan Structures: Syndicated loans can have complex structures and documentation, requiring experienced legal and financial advisors to navigate effectively. The borrower needs to fully understand the terms, covenants, and repayment obligations before entering into such an agreement.

– Relationship Management: Coordinating with multiple lenders and addressing their individual requirements during the loan administration phase requires efficient relationship management skills. Any conflicts or disagreements between lenders could impact the borrower’s relationship with the syndicate.

4.2 Lender’s Risks

– Credit Risk: Lenders bear the risk of borrower default or non-payment. While risk is mitigated through syndication, lenders still need to carefully assess the borrower’s creditworthiness and monitor their financial performance throughout the loan tenure.

– Market Liquidity: It may be challenging to sell or transfer loan portions in the secondary market, especially during periods of economic instability. Lenders should consider the potential impact on liquidity when participating in syndicated loans.

– Operational Risk: Participating lenders need efficient loan administration systems and processes to handle ongoing loan monitoring, interest payments, and potential amendments or waivers. Inadequate loan administration can lead to errors, delays, or even disputes among lenders.

In conclusion, syndicated loans serve as a vital financing option for borrowers in need of substantial capital. They provide access to a diverse network of lenders, flexible loan structures, and efficient execution. For lenders, syndicated loans offer risk diversification, exposure to new lending opportunities, and collaboration with other experienced financial entities. However, both borrowers and lenders should assess the associated risks and understand the complexities involved before entering into a syndicated loan agreement.

Syndicated Loans – What They Are and How They Work

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What is a syndicated loan?

A syndicated loan is a type of loan where multiple lenders provide funds to a borrower. It is typically used for large financing needs that reach beyond the capacity of a single lender.

How do syndicated loans work?

In a syndicated loan, one lead bank, known as the arranger, structures the loan and invites other banks to participate. The borrower receives the loan amount from all the participating lenders, who then share the risk and potential returns associated with the loan.

Who benefits from syndicated loans?

Syndicated loans benefit both borrowers and lenders. Borrowers gain access to larger loan amounts, while lenders have the opportunity to diversify their loan portfolios and earn interest income.

What are the advantages of syndicated loans?

Some advantages of syndicated loans include: access to larger loan amounts, spreading risk among multiple lenders, accessing expertise and resources of different lenders, and potentially obtaining more favorable loan terms.

What types of borrowers use syndicated loans?

Syndicated loans are commonly used by large corporations, financial institutions, and governments for various purposes such as mergers and acquisitions, project financing, working capital needs, and refinancing existing debt.

How are repayments made in syndicated loans?

Repayments in syndicated loans are typically structured in installments. The borrower makes periodic payments of both principal and interest to the lead arranger, who then distributes the funds proportionately among the participating lenders.

What role does the lead arranger play in syndicated loans?

The lead arranger in a syndicated loan takes on the responsibility of structuring the loan, negotiating terms, and coordinating the syndication process. They act as the main point of contact between the borrower and the lenders.

Can syndicated loans be traded in the secondary market?

Yes, syndicated loans can be traded in the secondary market. Lenders have the option to buy or sell their loan participations to other financial institutions, allowing for liquidity and potential profit or loss depending on market conditions.

Final Thoughts

Syndicated loans are a form of lending where a group of lenders jointly provides funds to a borrower. This allows borrowers to access larger sums of money than they would be able to secure from a single lender. Syndicated loans work by distributing the risk among the participating lenders, as they each contribute a portion of the total loan amount. These loans are often used for large-scale projects, mergers and acquisitions, or to finance a company’s growth. Overall, syndicated loans provide a flexible and efficient way for businesses to obtain the necessary capital for their endeavors.