Are you wondering about the tax implications of gifts and inheritance? Look no further! In this article, we will delve into the intricacies of how taxes are affected when it comes to receiving gifts or inheriting assets. Understanding these implications is crucial, as it can greatly impact your financial planning and decision-making. So, let’s dive right in and explore what you need to know about the tax implications of gifts and inheritance.

What Are the Tax Implications of Gifts and Inheritance?

When it comes to financial matters, understanding the tax implications is crucial. In the context of gifts and inheritance, there are specific rules and regulations that determine how taxes are applied. Whether you are giving or receiving gifts or inheriting assets, it’s important to be aware of these implications to make informed decisions. In this article, we will explore the various tax considerations associated with gifts and inheritance, providing you with valuable insights to navigate these financial transactions.

Gift Tax

1. Determining Gift Tax

Gift tax is a tax imposed on the transfer of assets from one individual to another without receiving equivalent value in return. The Internal Revenue Service (IRS) in the United States is responsible for implementing and regulating the gift tax. Understanding the following key aspects of gift tax can help you navigate this concept:

- Gift Tax Exclusion: As of 2021, the annual gift tax exclusion amount is $15,000 per recipient. This means that you can give up to $15,000 to an individual in a calendar year without incurring any gift tax. For married couples, this exclusion doubles to $30,000 per recipient.

- Cumulative Gift Tax Exemption: In addition to the annual exclusion, there is a lifetime gift tax exemption. As of 2021, the lifetime exemption stands at $11.7 million per individual. This means that any amount gifted over the annual exclusion will count towards the lifetime exemption. Once the lifetime exemption is exhausted, gift tax may apply.

- Gift Splitting: Married couples can choose to “split” gifts, combining their annual exclusions and doubling the amount they can give tax-free to each recipient. However, to utilize gift splitting, a gift tax return must be filed, even if no tax is owed.

- Exceptions to Gift Tax: Certain gifts are exempt from gift tax, including gifts to a spouse, qualified educational and medical expenses paid directly to the institution, and political organizations.

2. Reporting Gift Tax

If you make gifts that exceed the annual exclusion amount, you are required to report them to the IRS by filing a gift tax return. However, this doesn’t necessarily mean you will owe taxes. The gift tax return serves primarily as a mechanism to keep track of your lifetime exemption. It’s important to consult with a tax professional to ensure you comply with all reporting requirements.

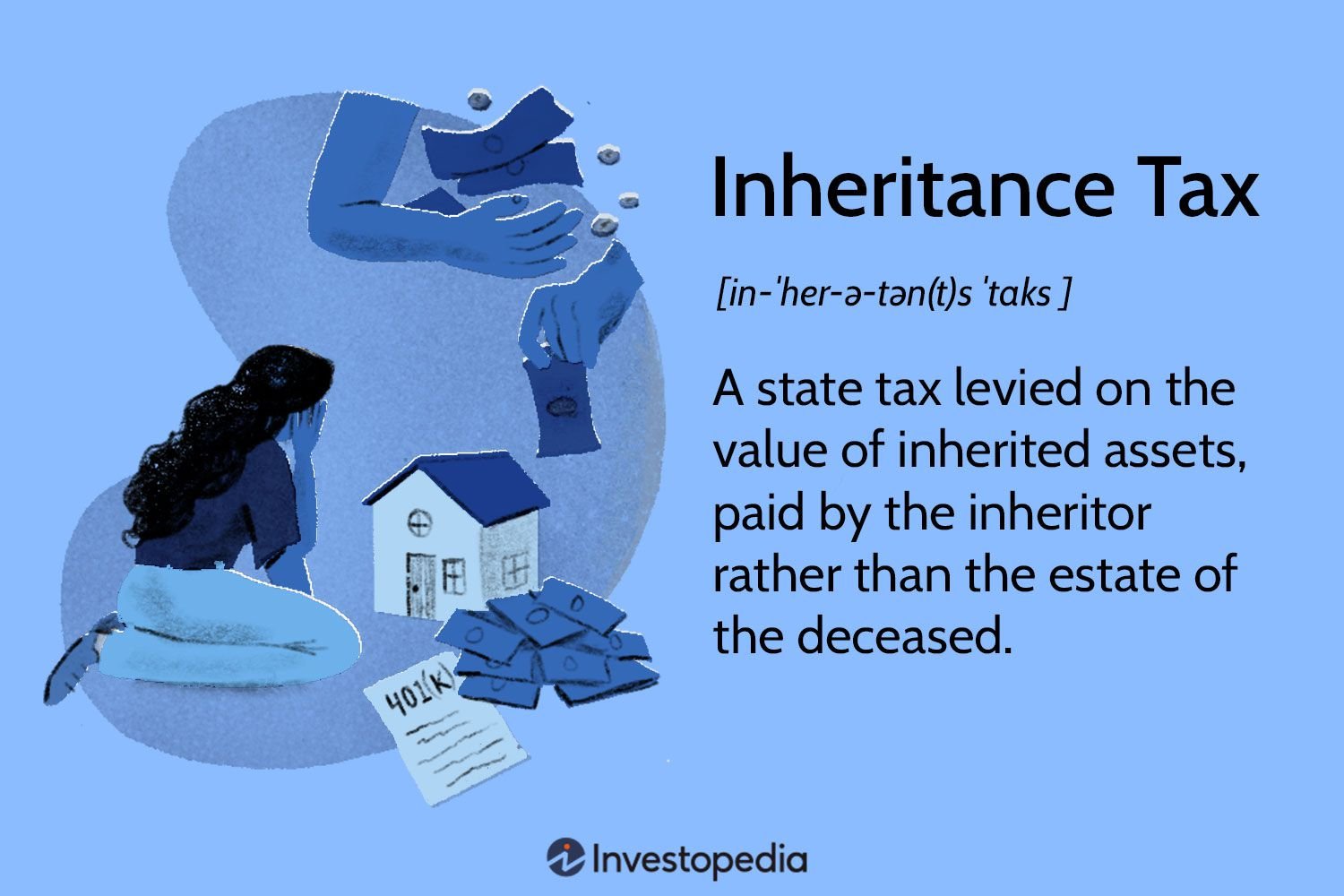

Inheritance Tax

1. Understanding Inheritance Tax

Inheritance tax is a tax imposed on the transfer of assets upon the death of an individual. Unlike gift tax, which is paid by the person making the gift, inheritance tax is typically paid by the individual receiving the assets. It’s essential to note that inheritance tax policies can vary significantly between jurisdictions, so it’s crucial to consult local tax laws and regulations. Here are a few key aspects to consider:

- Tax Exemptions and Thresholds: Many jurisdictions establish tax exemptions and thresholds that determine whether an inheritance is subject to tax. These thresholds vary depending on the relationship between the deceased and the heir. For example, spouses or direct descendants may have different tax exemptions compared to other individuals.

- Assets Subject to Tax: The types of assets subject to inheritance tax can vary. Common examples include real estate, investments, bank accounts, vehicles, and personal belongings. However, certain assets, such as life insurance proceeds or assets placed in trust, may be exempt from inheritance tax.

- Payment and Timing: Inheritance tax is typically due within a specific period after the date of death. The heir or executor of the estate is responsible for ensuring the tax is paid in a timely manner.

- International Considerations: Inheritance tax can become more complex when assets and individuals involved are located in different countries. In such cases, it’s crucial to seek professional advice to navigate the intricacies of international tax laws.

Capital Gains Tax

1. Capital Gains Tax on Gifts and Inherited Assets

In addition to gift and inheritance tax, it’s essential to consider the implications of capital gains tax when you dispose of assets received through gifts or inheritance. Capital gains tax is a tax on the profit earned from the sale of an asset. Here’s what you need to know:

- Cost Basis Adjustment: When you receive an asset through a gift or inheritance, the cost basis for determining capital gains tax is generally adjusted. The cost basis is the original value of the asset for tax purposes, and the adjustment is based on the fair market value at the time of the gift or the date of death of the original owner.

- Capturing Capital Gains: If you sell an inherited or gifted asset and realize a capital gain, you will be subject to capital gains tax. The tax rate can vary depending on factors such as your income level, the type of asset, and the duration of ownership.

- Step-Up in Basis: In some jurisdictions, inherited assets may benefit from a step-up in basis. This means that the cost basis is adjusted to the fair market value at the date of death, helping to minimize potential capital gains taxes when the asset is sold.

Qualified Plans and IRAs

1. Tax Considerations for Qualified Plans and IRAs

Qualified retirement plans, such as 401(k)s, and Individual Retirement Accounts (IRAs) have their own set of tax implications when it comes to gifting and inheritance. Here’s what you should know:

- Required Minimum Distributions (RMDs): If you inherit a qualified plan or IRA, you may be subject to required minimum distributions based on your relationship to the original account holder and their age at the time of their passing. Failure to take the required distributions may result in penalties.

- Stretch IRAs: In the past, beneficiaries had the option to “stretch” the distributions over their lifetime. However, recent changes in tax legislation have limited this option for many beneficiaries, requiring them to distribute the assets within ten years of the original account holder’s death.

- Spousal Rollovers: Spouses who inherit qualified plans or IRAs may be eligible for a rollover, allowing them to postpone distributions until they reach the mandatory distribution age.

- Beneficiary Designations: Reviewing and updating beneficiary designations on qualified plans and IRAs is crucial to ensure the smooth transfer of assets and potentially minimize tax consequences.

Seeking Professional Advice

1. The Importance of Professional Guidance

Given the complexity of tax laws and regulations surrounding gifts and inheritance, consulting with a qualified tax professional is highly recommended. They can provide expert guidance tailored to your specific situation and help you navigate the intricacies of tax implications. Some of the benefits of seeking professional advice include:

- Tax Planning: Professionals can help you develop tax-efficient strategies for gifting, inheritance, and asset disposition, potentially saving you money in the long run.

- Compliance: Tax professionals ensure that you comply with all reporting requirements and meet relevant deadlines, reducing the risk of penalties or legal complications.

- Maximizing Exemptions: Experts can help you leverage available exemptions and deductions, ensuring you make the most of your gift and inheritance tax planning.

In conclusion, understanding the tax implications of gifts and inheritance is essential for effective financial planning. By grasping the basics of gift tax, inheritance tax, capital gains tax, and the nuances of qualified plans and IRAs, you can make informed decisions that align with your financial goals. While this article provides a comprehensive overview, it’s crucial to consult with a tax professional to navigate your specific circumstances and ensure compliance with applicable laws and regulations.

In America – Gift vs trust inheritance

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What are the tax implications of gifts and inheritance?

When it comes to gifts and inheritance, there are certain tax implications to be aware of. Here are some frequently asked questions related to this topic:

1. Are gifts taxable?

Gifts are generally not taxable for the recipient. However, the person making the gift may be subject to gift tax if the total amount of gifts made in a year exceeds the annual gift tax exclusion set by the tax authorities.

2. What is the annual gift tax exclusion?

The annual gift tax exclusion is the maximum amount of money or property that can be gifted to another person without incurring any gift tax. This exclusion amount is subject to change and it’s recommended to check with the latest tax regulations for the specific year.

3. Do I need to report gifts on my tax return?

Generally, you don’t need to report gifts received on your tax return. The responsibility to report and potentially pay gift tax lies with the person making the gift. However, if you receive a gift from a foreign person or entity, there might be reporting requirements.

4. What happens if the value of a gift exceeds the annual gift tax exclusion?

If the value of a gift exceeds the annual gift tax exclusion, the person making the gift may need to file a gift tax return. However, most individuals have a lifetime exemption, which allows them to make gifts over the annual exclusion without paying gift tax.

5. Are there any tax implications for inherited property?

Inherited property is generally not subject to income tax for the recipient. However, if you sell the inherited property, you may need to pay capital gains tax on any appreciation in value from the time of inheritance to the time of sale.

6. What is the stepped-up basis for inherited property?

The stepped-up basis refers to the fair market value of the inherited property at the time of the original owner’s death. When you inherit property, your tax basis is generally “stepped up” to this fair market value, which can reduce the amount of capital gains tax you may owe if you sell the property.

7. Can I deduct the gift or inheritance on my income tax return?

No, gifts and inheritances are not deductible on your income tax return. These transfers of wealth are not considered taxable income to the recipient.

8. Are there any specific rules for gifts and inheritances from abroad?

Gifts and inheritances from abroad may have specific tax implications. It’s important to consult with a tax professional or refer to the tax laws of your country to understand any reporting or tax obligations that may apply in these situations.

Final Thoughts

In conclusion, it is important to understand the tax implications of gifts and inheritance. When receiving a gift, it is generally not subject to tax for the recipient. However, the person giving the gift may be subject to gift tax if the amount exceeds a certain threshold. In the case of inheritance, the recipient is typically not taxed on the inherited assets. However, any income generated from those assets may be subject to income tax. It is crucial to consult with a tax professional to ensure compliance with relevant tax laws and properly manage any tax obligations. Understanding the tax implications of gifts and inheritance is essential for effective financial planning and asset management.