Curious about financial guarantees in loans? Wondering how they work and what role they play in the lending process? Look no further! In this blog article, we’ll dive into the concept of a financial guarantee in loans and shed light on its importance. Whether you’re a borrower or simply interested in understanding how loans work, this article will provide you with a comprehensive explanation of what a financial guarantee in loans entails. So, let’s get started and demystify the world of financial guarantees!

What is a Financial Guarantee in Loans?

When it comes to borrowing money, lenders often require some form of assurance that they will be repaid. This is where a financial guarantee in loans comes into play. A financial guarantee is a contractual agreement between a borrower, a lender, and a third party, known as the guarantor. The guarantor agrees to assume responsibility for the loan if the borrower fails to meet their repayment obligations.

Financial guarantees provide lenders with an extra layer of security, reducing the risk of default and potential financial loss. They give lenders the confidence to lend money to borrowers who may not meet the typical credit requirements on their own. Guarantees can take various forms, including personal guarantees, corporate guarantees, and even government guarantees.

Types of Financial Guarantees

There are several types of financial guarantees that borrowers can utilize to secure a loan. These include:

- Personal Guarantees: A personal guarantee is an agreement where an individual assumes responsibility for the loan if the borrower defaults. In this type of guarantee, the guarantor’s personal assets are at risk.

- Corporate Guarantees: Corporate guarantees involve a company assuming responsibility for the loan on behalf of an individual or another company. In this case, the guarantor’s assets are typically not at risk, and the lender relies on the financial strength of the corporation.

- Government Guarantees: Government guarantees are provided by the government to support specific types of loans, such as small business loans or home loans. These guarantees offer lenders additional protection and encourage them to provide financing to borrowers who may not meet traditional lending criteria.

Benefits of Financial Guarantees

Financial guarantees offer several benefits to both lenders and borrowers, including:

- Increased Access to Credit: Financial guarantees open up borrowing opportunities for individuals or businesses that may not qualify for a loan based solely on their own creditworthiness. This expands access to credit and fosters economic growth.

- Lower Interest Rates: Lenders may offer lower interest rates to borrowers who provide a financial guarantee. The reduced risk of default associated with the guarantee allows lenders to provide more favorable loan terms.

- Flexible Loan Terms: Financial guarantees can help borrowers negotiate more flexible loan terms, such as longer repayment periods or deferred payment options.

- Building Credit History: For borrowers with limited or poor credit history, a financial guarantee can help establish or improve their creditworthiness. Making timely payments on a guaranteed loan can have a positive impact on their credit score.

- Supporting Economic Initiatives: Government guarantees play a crucial role in supporting various economic initiatives. They promote lending to specific sectors or demographics, such as small businesses or first-time homebuyers.

Responsibilities of the Parties Involved

When a financial guarantee is in place, each party involved has specific responsibilities:

- Borrower: The borrower is responsible for meeting the loan repayment obligations as outlined in the loan agreement. Failure to repay the loan may result in the guarantor assuming the responsibility and potentially pursuing legal action against the borrower.

- Lender: The lender provides the loan to the borrower and evaluates the creditworthiness of the borrower and guarantor (if applicable). The lender must also monitor the loan repayment and take appropriate action in case of default.

- Guarantor: The guarantor assumes the responsibility for the loan if the borrower defaults. This involves repaying the outstanding balance, including any accrued interest and fees. The guarantor’s level of liability depends on the type of guarantee provided.

Factors to Consider Before Providing a Financial Guarantee

Before agreeing to provide a financial guarantee, it’s essential for potential guarantors to consider several factors:

- Financial Stability: Guarantors need to assess their own financial stability and ability to fulfill the guarantee obligations if necessary. They should ensure they have sufficient assets or income to cover any potential liabilities.

- Relationship with the Borrower: Consider the strength of the relationship with the borrower. Providing a financial guarantee typically involves trust and, in many cases, a close personal or professional connection.

- Risk Assessment: Evaluate the borrower’s creditworthiness and the associated risks. Understand the purpose of the loan, the borrower’s ability to repay, and any collateral available to secure the loan.

- Legal and Financial Advice: Seek professional advice, such as legal or financial counsel, to fully understand the implications of providing a financial guarantee. They can guide potential guarantors through the process and ensure they are aware of their rights and obligations.

In conclusion, a financial guarantee in loans serves as a safety net for lenders, providing them with added security when extending credit. Various types of financial guarantees exist, including personal guarantees, corporate guarantees, and government guarantees. These guarantees offer benefits to borrowers, such as increased access to credit and favorable loan terms. However, it’s crucial for potential guarantors to carefully consider their financial stability and seek professional advice before providing a guarantee. By understanding the responsibilities and risks associated with financial guarantees, borrowers and guarantors can navigate the lending process confidently.

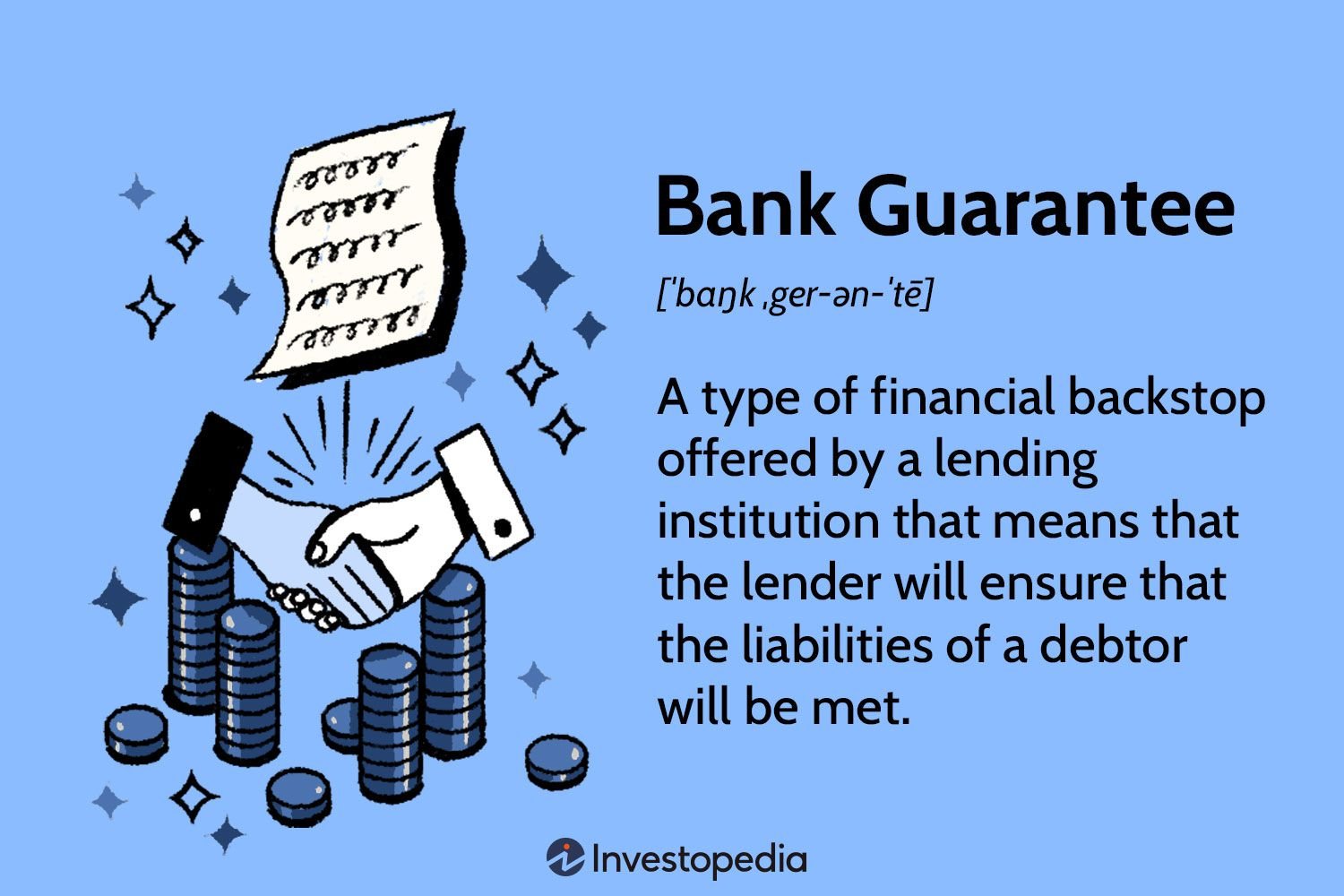

What is a Bank Guarantee?

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What is a financial guarantee in loans?

A financial guarantee in loans refers to a commitment made by a person or an organization to assume the responsibility of repaying a loan in case the borrower is unable to fulfill their financial obligations. It acts as a form of assurance to the lender that they will be protected from losses.

How does a financial guarantee work?

When a financial guarantee is provided for a loan, the guarantor becomes legally bound to repay the outstanding debt if the borrower defaults. Lenders often require a financial guarantee when they perceive a higher risk associated with the borrower. In such cases, the guarantor’s assets can be used to repay the loan.

Who can provide a financial guarantee?

A financial guarantee can be provided by individuals, companies, or even third-party institutions depending on the loan agreement. Guarantors are usually required to have a stable financial position and a good credit history to ensure their ability to fulfill the guarantee.

What are the types of financial guarantees?

There are several types of financial guarantees in loans, including:

1. Personal Guarantees: These guarantees involve an individual taking personal responsibility for loan repayment.

2. Corporate Guarantees: In this case, a company guarantees repayment on behalf of another company or individual.

3. Joint Guarantees: Multiple individuals or entities jointly guarantee repayment of a loan.

4. Limited Guarantees: Guarantees that are only applicable up to a certain amount or for a specific duration.

Can a financial guarantee affect the credit score of the guarantor?

Yes, a financial guarantee can impact the credit score of the guarantor. If the primary borrower fails to repay the loan, it may reflect negatively on the guarantor’s credit history. It is essential for the guarantor to ensure that the borrower fulfills their obligations to avoid any negative consequences.

What are the risks associated with being a financial guarantor?

As a financial guarantor, there are several risks involved, including:

1. Financial Liability: If the borrower defaults, the guarantor becomes legally responsible for repaying the loan.

2. Credit Risk: Guarantors’ credit ratings may be affected if the borrower fails to make timely payments.

3. Legal Consequences: In case of loan default, lenders may take legal action against the guarantor to recover the outstanding debt.

Can a financial guarantee be revoked?

In some cases, a financial guarantee can be revoked if both parties agree to the cancellation and the loan agreement allows for such revocation. However, it is essential to carefully review the terms and conditions of the loan agreement before assuming the guarantee can be revoked.

Are there any alternatives to providing a financial guarantee?

Yes, there are alternatives to providing a financial guarantee, such as:

1. Collateral: Instead of relying on a guarantor, borrowers can provide collateral, such as property or assets, to secure the loan.

2. Improving Creditworthiness: Borrowers can work on improving their creditworthiness by maintaining a good credit history and demonstrating a stable financial position, reducing the need for a financial guarantee.

Please note that the specific terms and conditions of financial guarantees may vary depending on the loan agreement and the lender’s requirements. It is always advisable to consult with a financial advisor or legal expert for personalized advice.

Final Thoughts

A financial guarantee in loans is a form of assurance provided by a third party, such as a bank or insurance company, to support the repayment of a loan. It serves as a commitment to cover the borrower’s liabilities in the event of default. This guarantee can provide lenders with increased confidence to extend loans to individuals or businesses that may otherwise be deemed too risky. By offering this assurance, financial institutions aim to mitigate potential losses and safeguard their interests. Understanding the concept of a financial guarantee in loans is crucial for borrowers and lenders alike in order to make informed decisions regarding financing options and risk management strategies.