Are you familiar with a health savings account (HSA)? Wondering what it entails and how it could benefit you? Look no further! In this blog article, we’ll explore the ins and outs of HSAs, helping you understand their purpose, advantages, and how they can support your healthcare needs. Whether you’re seeking ways to save money on medical expenses or striving for a more proactive approach to managing your well-being, an HSA could be the solution you’ve been searching for. So, let’s dive in and uncover the world of health savings accounts together!

What is a Health Savings Account (HSA)?

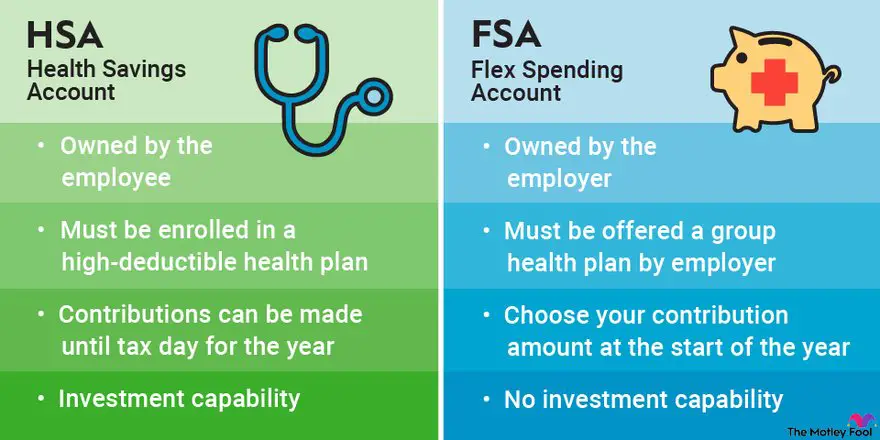

A Health Savings Account (HSA) is a type of tax-advantaged savings account that allows individuals and families to save money specifically for medical expenses. It is available to those who have a high-deductible health insurance plan (HDHP). The funds contributed to an HSA are tax-deductible, grow tax-free, and can be withdrawn tax-free when used for qualified medical expenses.

How Does an HSA Work?

Understanding how an HSA works is essential for maximizing its benefits. Here’s a breakdown of the key elements:

- Eligibility: To open and contribute to an HSA, you must be enrolled in a high-deductible health plan (HDHP). The specific requirements for an HDHP may vary, but it typically means having a higher deductible and out-of-pocket maximum compared to traditional health insurance plans.

- Contributions: The money you contribute to your HSA is tax-deductible, meaning it reduces your taxable income. The annual contribution limits are set by the IRS and may change each year. For 2021, the maximum contribution is $3,600 for individuals and $7,200 for families. Additionally, individuals aged 55 and older can make an additional catch-up contribution of $1,000.

- Tax Advantages: One of the biggest advantages of an HSA is its tax benefits. Not only are contributions tax-deductible, but the growth of your HSA funds is tax-free. Additionally, when you withdraw money from your HSA to pay for qualified medical expenses, those withdrawals are also tax-free.

- Qualified Medical Expenses: HSAs can be used to pay for a wide range of qualified medical expenses, including doctor visits, prescription medications, hospital stays, and medical procedures. The IRS provides a comprehensive list of qualified expenses, but it’s important to note that not all healthcare expenses may be covered.

- Portability: Unlike Flexible Spending Accounts (FSAs), HSAs are not subject to the “use it or lose it” rule. The money in your HSA rolls over from year to year, allowing you to accumulate funds for future medical expenses. HSAs are also portable, meaning they stay with you even if you change jobs or health insurance plans.

The Benefits of Having an HSA

Health Savings Accounts offer numerous benefits that make them an attractive option for individuals and families. Here are some key advantages of having an HSA:

- Tax Savings: Contributions to an HSA are tax-deductible, reducing your taxable income. Any interest or investment gains on the funds in your HSA are tax-free, and withdrawals for qualified medical expenses are also tax-free. These tax advantages can add up significantly over time.

- Control and Flexibility: With an HSA, you have control over how you spend your healthcare dollars. You can use the funds to pay for a wide range of qualified medical expenses, including those not typically covered by insurance, such as dental and vision care. This flexibility allows you to tailor your healthcare decisions based on your specific needs.

- Savings and Investment Opportunities: HSAs can be an effective way to save and invest for future healthcare expenses. Some HSA providers offer investment options, allowing you to grow your HSA funds over time. By investing wisely, you can potentially increase your savings and have more funds available for healthcare needs in the future.

- Portability: As mentioned earlier, HSAs are portable, which means you can keep your account even if you change jobs or health insurance plans. This gives you the freedom to continue using and contributing to your HSA, regardless of your employment situation.

- Long-Term Savings Potential: HSAs can serve as a valuable long-term savings tool. While the primary purpose is to cover current and future medical expenses, HSAs can also be used as a retirement savings vehicle. Once you turn 65, you can withdraw funds from your HSA for any reason without incurring the 20% penalty typically associated with non-medical withdrawals. However, non-medical withdrawals are still subject to income tax.

Drawbacks and Considerations of HSAs

While Health Savings Accounts offer many benefits, there are also some drawbacks and considerations to keep in mind:

- High-Deductible Health Plan Requirement: To qualify for an HSA, you must have a high-deductible health plan (HDHP). This means you may be responsible for a larger portion of your healthcare costs upfront before your insurance coverage kicks in. It’s important to assess your healthcare needs and financial situation to ensure an HDHP is the right choice for you.

- Contribution Limits: Although HSAs offer tax advantages, there are annual contribution limits set by the IRS. It’s important to understand and adhere to these limits, as contributing more than the allowable amount may result in tax penalties.

- Qualified Medical Expenses: While HSAs cover a wide range of medical expenses, not all healthcare costs are considered qualified expenses. You must ensure that the expenses you plan to use your HSA funds for are eligible. The IRS provides a list of qualified medical expenses, or you can consult with a tax professional for guidance.

- Account Fees: Some HSA providers may charge fees for account maintenance, transactions, or investment options. It’s essential to compare different HSA providers and understand the potential fees associated with each before opening an account.

- Coordination with Other Healthcare Accounts: If you have other healthcare accounts, such as a Flexible Spending Account (FSA) or Health Reimbursement Arrangement (HRA), it’s important to understand how they interact with your HSA. There may be guidelines or restrictions on using multiple accounts together, so it’s advisable to review your plan documents or consult with your benefits administrator.

Maximizing the Benefits of Your Health Savings Account

To make the most of your Health Savings Account, consider implementing the following strategies:

- Contribute Regularly: Aim to contribute the maximum allowable amount to your HSA each year. Regular contributions will help grow your savings and provide a cushion for future medical expenses.

- Invest Wisely: If your HSA offers investment options, consider allocating a portion of your funds to investments that align with your long-term goals. However, be mindful of the risks associated with investments and ensure you have a sufficient balance to cover near-term healthcare costs.

- Track and Save Receipts: Keep track of all medical receipts and expenses that you pay out of pocket. This documentation will be valuable if you need to substantiate your withdrawals and demonstrate that they were for qualified medical expenses.

- Use HSA for Long-Term Planning: As you approach retirement, consider shifting your HSA strategy to incorporate long-term planning. Since HSA withdrawals for non-medical expenses are subject to income tax after age 65, your HSA funds can be used as an additional source of retirement income.

- Stay Informed: Familiarize yourself with the latest rules and regulations regarding HSAs. Healthcare laws may change over time, so it’s essential to stay informed and make informed decisions about your HSA.

A Health Savings Account can be a valuable tool for managing healthcare costs and providing financial security. By understanding how HSAs work, their benefits, drawbacks, and strategic tips for maximizing their advantages, you can make informed decisions and take full advantage of this powerful savings vehicle.

What is a Health Savings Account? HSA Explained for Dummies

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What is a Health Savings Account (HSA)?

A Health Savings Account (HSA) is a tax-advantaged savings account that individuals can use to save money for qualified medical expenses. It is typically paired with a high-deductible health plan (HDHP) and offers various benefits, such as tax deductions, tax-free growth, and the ability to withdraw funds for healthcare expenses without incurring taxes.

How does a Health Savings Account (HSA) work?

With an HSA, individuals can contribute pre-tax money from their paycheck or make after-tax contributions. The funds in the account can be used to pay for qualified medical expenses, including doctor visits, prescription medications, and certain medical devices. These contributions and withdrawals are tax-free, allowing individuals to save on healthcare costs.

Who is eligible for a Health Savings Account (HSA)?

To be eligible for an HSA, you must be enrolled in a high-deductible health plan (HDHP). Additionally, you must not be covered by any other non-HDHP health plan, not be enrolled in Medicare, and not be claimed as a dependent on someone else’s tax return. Eligibility requirements may vary, so it’s advisable to check with your employer or the HSA provider.

What are the benefits of having a Health Savings Account (HSA)?

Having an HSA offers several benefits. Firstly, contributions made to the account are tax-deductible, reducing your taxable income. The funds in the account can grow tax-free through investments, providing an opportunity for long-term savings. Additionally, withdrawals used for qualified medical expenses are tax-free. HSAs also offer flexibility, as the funds can be carried over from year to year and can be used to pay for a wide range of healthcare expenses.

How much can I contribute to a Health Savings Account (HSA)?

The contribution limits for HSAs are determined annually by the IRS. For 2021, the limit for individuals with self-only coverage is $3,600, while the limit for individuals with family coverage is $7,200. If you are 55 years or older, you may be eligible to make additional catch-up contributions.

Can I use my Health Savings Account (HSA) funds for non-medical expenses?

While HSAs are primarily designed for qualified medical expenses, there are certain exceptions. If you withdraw funds for non-medical expenses before the age of 65, you will be subject to income taxes and an additional 20% penalty. However, once you reach the age of 65, you can withdraw funds for any purpose without incurring the penalty, although income taxes may still apply.

Can I invest the funds in my Health Savings Account (HSA)?

Yes, many HSA providers offer the option to invest the funds in your account. This allows you to potentially grow your savings by investing in mutual funds, stocks, and other investment options. However, it’s important to note that investment options and potential returns may vary depending on the provider.

What happens to my Health Savings Account (HSA) if I change jobs or retire?

If you change jobs or retire, your HSA remains yours. You can continue to use the funds for qualified medical expenses, even if you are no longer enrolled in a high-deductible health plan. Additionally, you can still contribute to the account as long as you meet the eligibility requirements. It’s a portable savings account that stays with you throughout your healthcare journey.

Final Thoughts

A Health Savings Account (HSA) is a financial tool that allows individuals to save money for medical expenses. It is a tax-advantaged account that offers individuals more control over their healthcare expenses. With an HSA, individuals can contribute pre-tax dollars, which can then be used to pay for qualified medical expenses. The funds in an HSA can be invested and grow over time. Moreover, any unused funds roll over from year to year, making it a long-term savings option. HSAs also offer flexibility as they are portable and can be used even if an individual changes jobs or health insurance plans. In summary, a Health Savings Account (HSA) is a valuable tool that empowers individuals to take control of their healthcare expenses and save for the future.