Are you curious about what a mezzanine loan in real estate entails? Well, look no further! This blog article will provide you with a clear understanding of what a mezzanine loan is and how it functions within the real estate industry. So, let’s dive right in and explore this intriguing concept. A mezzanine loan in real estate refers to a secondary loan that sits between the senior debt and the equity in a property transaction. This means that it has characteristics of both debt and equity, offering unique advantages to both borrowers and investors. Let’s unravel the details!

What is a Mezzanine Loan in Real Estate?

Real estate investments often require substantial capital, and sometimes traditional financing options may not cover the entire cost. In such cases, investors turn to alternative sources of funding, one of which is a mezzanine loan.

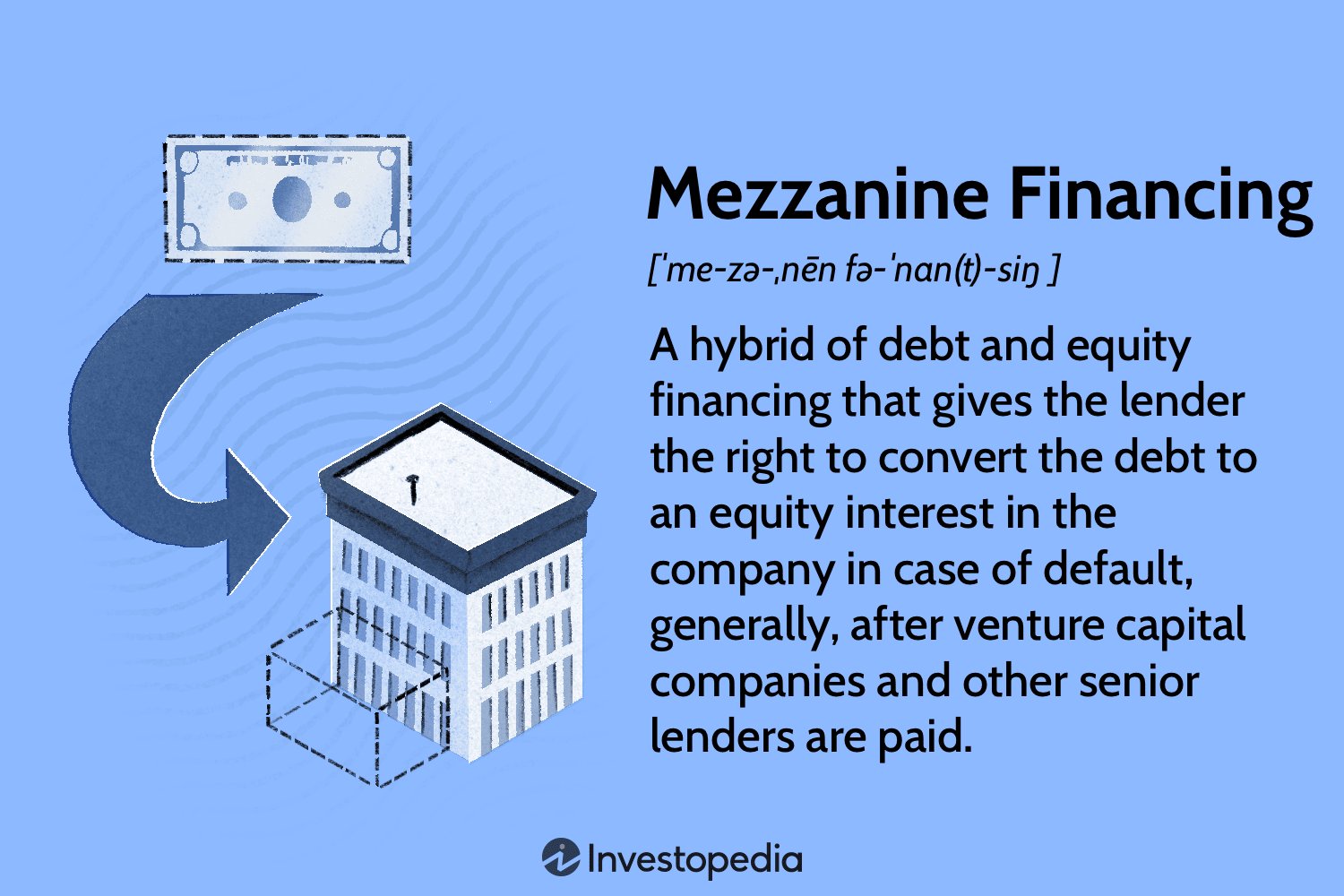

A mezzanine loan is a unique form of financing that fills the gap between the equity invested and the senior debt secured against a property. It is commonly used in commercial real estate transactions, especially for large-scale developments or acquisitions. This type of loan serves as a second lien on the property and ranks below the senior debt but above the equity investment.

Mezzanine loans are typically structured as flexible, short- to medium-term loans with higher interest rates compared to senior debt. They offer investors an opportunity to access additional capital for their real estate projects while minimizing the need for additional equity investment. Let’s explore the various aspects of mezzanine loans in real estate in more detail.

The Role of Mezzanine Loans in Real Estate Financing

Mezzanine loans play a crucial role in real estate financing by bridging the gap between the senior debt and the equity investment. This type of financing is often used when the available equity investment falls short of the total capital required for a project. Here are some key points explaining the role of mezzanine loans:

1. Supplementing the Equity Gap: Mezzanine loans provide developers and investors with additional capital necessary to complete real estate projects. By securing this financing, they can avoid diluting their ownership stake or seeking additional equity investors.

2. Reducing the Need for Additional Equity: By opting for a mezzanine loan, borrowers can reduce the amount of equity they need to contribute. This can be particularly beneficial when the available equity is limited or when investors want to retain a larger portion of the ownership.

3. Enabling Larger Real Estate Projects: Mezzanine loans allow developers to undertake larger and more complex projects by providing the necessary funding beyond the senior debt. This helps unlock potential returns and maximize the value of the investment.

The Mechanics of Mezzanine Loans

Understanding the mechanics of mezzanine loans can help investors make informed decisions when considering this form of financing. Here are the key aspects of mezzanine loans in real estate:

1. Subordinate Position: A mezzanine loan is a junior loan that ranks below the senior mortgage but above the equity investment. In case of default or foreclosure, the senior debt holders are paid off first, followed by the mezzanine lender and then the equity investors.

2. Increased Risk and Return: Mezzanine loans carry higher interest rates compared to senior debt due to the increased risk associated with their subordinate position. Investors accepting this risk are rewarded with a higher potential return on their investment.

3. Collateral: Mezzanine loans are generally secured by pledges of equity interests or ownership stakes in the borrowing entity (typically a special purpose vehicle). This collateral provides additional security to the lender in case of default.

4. Loan Terms: Mezzanine loans are typically structured as interest-only loans with a balloon payment due at the end of the term. The loan term is usually shorter than the senior debt, ranging from three to seven years.

5. Loan-to-Value Ratio (LTV): The loan-to-value ratio of a mezzanine loan is higher than that of the senior debt but lower than the total value of the property. LTV ratios for mezzanine loans often range between 70% and 90%.

Benefits and Drawbacks of Mezzanine Loans

As with any form of financing, mezzanine loans come with their own set of advantages and disadvantages. It’s important to evaluate these factors when considering whether a mezzanine loan is suitable for a real estate project. Let’s explore the benefits and drawbacks:

1. Benefits of Mezzanine Loans:

– Additional Capital: Mezzanine loans provide access to additional capital, allowing investors to pursue larger or more ambitious real estate projects.

– Potential for Higher Returns: By leveraging the project’s potential returns with borrowed funds, investors have the opportunity to achieve higher overall returns on their investment.

– Preservation of Equity Ownership: Mezzanine loans enable investors to retain a larger ownership stake in the project by reducing the amount of required equity investment.

– Flexible Structuring: Mezzanine loans can be tailored to fit specific project requirements, offering flexibility in terms of interest rates, repayment terms, and other key aspects.

2. Drawbacks of Mezzanine Loans:

– Higher Costs: Mezzanine loans typically carry higher interest rates and additional fees compared to senior debt, increasing the overall cost of financing for the borrower.

– Increased Risk: Mezzanine loans are subordinate to senior debt, meaning that in case of default or foreclosure, the mezzanine lender bears a higher risk of not fully recovering their investment.

– Limited Availability: Mezzanine financing is not as readily available as senior debt, and its availability may be subject to market conditions and the borrower’s creditworthiness.

– Complex Structuring: The structuring and documentation of mezzanine loans can be complex, requiring legal expertise and detailed negotiations between parties involved.

Key Considerations for Borrowers and Lenders

Both borrowers and lenders must take various factors into account when engaging in mezzanine financing. Here are some key considerations for these stakeholders:

1. Borrowers:

– Project Viability: Borrowers should thoroughly assess the viability of the real estate project before pursuing mezzanine financing. A robust business plan and comprehensive market analysis are essential for attracting potential lenders.

– Cost-Benefit Analysis: Conducting a cost-benefit analysis is crucial to determine whether the additional costs associated with mezzanine financing are justified by the potential returns and project profitability.

– Repayment Strategy: Borrowers should carefully plan their repayment strategies, considering both the interest payments during the loan term and the balloon payment at the end. Exploring refinancing options in advance can provide additional flexibility.

2. Lenders:

– Due Diligence: Lenders must conduct thorough due diligence on the borrower, the project, and the collateral offered. This includes evaluating the borrower’s financial stability, project feasibility, and potential risks.

– Loan Structuring: Lenders should carefully structure the mezzanine loan, taking into account the project’s timeline, expected cash flows, and other relevant factors. A well-structured loan can mitigate risks and maximize returns.

– Legal Considerations: Engaging legal counsel is important for lenders to ensure that the loan agreements and collateral arrangements are properly drafted and enforceable.

– Risk Management: Lenders should assess the risk associated with mezzanine loans, including the market conditions, project-specific risks, and the borrower’s creditworthiness. Implementing effective risk management strategies is crucial.

In conclusion, mezzanine loans offer a valuable financing option for real estate projects, enabling developers and investors to access additional capital while minimizing the need for additional equity investment. By understanding the role, mechanics, benefits, and drawbacks of mezzanine loans, borrowers and lenders can make informed decisions and mitigate risks. However, it is important to carefully evaluate the specific circumstances of each project and seek professional advice to ensure a successful financing arrangement.

Mezzanine Loans | Mezzanine Financing in Real Estate Explanation with Example

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What is a mezzanine loan in real estate?

A mezzanine loan in real estate refers to a type of financing that sits between the senior debt (usually provided by a traditional lender) and the equity investment. It is a form of secondary financing where the lender has the right to convert their loan into equity ownership in the property if the borrower defaults on payments. Mezzanine loans are often used to bridge the gap between the amount of senior debt available and the total project cost.

How does a mezzanine loan differ from traditional financing?

Unlike traditional financing, mezzanine loans are typically unsecured and carry higher interest rates. They are subordinate to senior debt and have a lower priority of payment in case of default. Mezzanine lenders also have the option to participate in the project’s profits through equity ownership.

What are the benefits of using a mezzanine loan in real estate?

Mezzanine loans offer several advantages in real estate transactions. They provide developers with additional capital to complete their projects, allowing them to take on larger or more complex ventures. Mezzanine financing can also enhance the developer’s return on investment by leveraging their equity with borrowed capital.

Who typically provides mezzanine loans in real estate?

Mezzanine loans are commonly offered by specialized lenders or investment firms that focus on real estate financing. These lenders have expertise in evaluating the risks and potential returns associated with mezzanine financing.

How is the interest rate determined for a mezzanine loan?

The interest rate for a mezzanine loan is typically higher than that of senior debt due to the increased risk involved. The rate is influenced by factors such as the project’s location, the borrower’s creditworthiness, and the loan-to-value ratio. The lender may also consider the borrower’s track record and the overall market conditions.

What are the key terms and conditions of a mezzanine loan?

The terms and conditions of a mezzanine loan can vary depending on the lender and the specific project. Some common terms include the loan-to-value ratio, the loan term, the repayment structure, default provisions, and conversion rights. It is important for borrowers to carefully review and negotiate these terms before entering into a mezzanine loan agreement.

What happens if the borrower defaults on a mezzanine loan?

In the event of a default on a mezzanine loan, the lender may have the right to initiate a foreclosure process and take ownership of the property. Depending on the terms of the loan agreement, the lender may also have the option to convert the loan into equity and become a partial owner of the property.

Can mezzanine loans be used for both residential and commercial real estate?

Yes, mezzanine loans can be utilized for both residential and commercial real estate projects. Whether it’s a large-scale commercial development or a residential condominium project, developers can explore mezzanine financing options to supplement their other sources of capital.

Final Thoughts

A mezzanine loan is a financing option in the real estate industry that bridges the gap between senior debt and equity. It is a form of subordinate debt that provides flexibility and additional capital for property development or ownership. Mezzanine loans are typically used for large-scale projects and offer higher returns for investors due to the increased risk involved. These loans are secured by a share of the property’s ownership and are often used to leverage other financing options. In summary, a mezzanine loan in real estate serves as a valuable financial tool that enables developers and property owners to access additional funding for their ventures.