Curious about what an interest-only mortgage loan is? Look no further! In this article, we’ll delve into the world of interest-only mortgage loans and decipher how they work. Picture this: instead of paying both the principal and interest on your mortgage, you have the option to pay just the interest for a certain period. Sounds intriguing, right? Well, let’s explore the ins and outs of interest-only mortgage loans, from their features to their pros and cons. So, what exactly is an interest-only mortgage loan? Let’s find out!

What is an Interest-Only Mortgage Loan?

When it comes to getting a mortgage, there are various options available to homebuyers. One popular choice is an interest-only mortgage loan, which offers unique advantages and considerations for borrowers. In this article, we will delve into the details of interest-only mortgages, exploring how they work, their benefits, potential drawbacks, and why they may or may not be the right choice for you.

Understanding the Basics

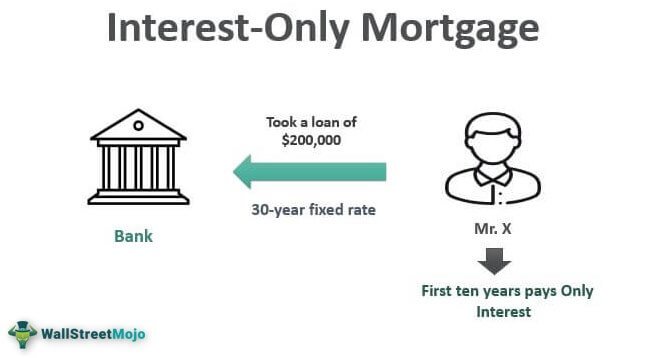

An interest-only mortgage loan is a type of loan where the borrower is only required to pay the interest on the loan for a certain period, typically for the first few years. This means that during this period, the monthly mortgage payments are considerably lower compared to a traditional mortgage loan, where both principal and interest are paid each month.

However, it’s important to note that the interest-only period is usually temporary, typically ranging from five to ten years. After this initial period, the loan structure changes, and the borrower is required to start making payments towards both the principal and the remaining interest.

The Benefits of an Interest-Only Mortgage Loan

Interest-only mortgages offer several potential benefits that can make them an attractive option for certain borrowers. Let’s take a closer look at these advantages:

- Lower Initial Payments: One of the biggest advantages of an interest-only mortgage loan is the lower monthly payments during the initial period. This can provide borrowers with more flexibility in managing their finances and allow for additional discretionary income.

- Investment Opportunities: By choosing an interest-only mortgage, borrowers may have more funds available to invest elsewhere, such as in stocks, business ventures, or other real estate opportunities. This can potentially lead to higher returns on investment.

- Higher Loan Amount: Since the initial monthly payments are lower, borrowers may be eligible for a higher loan amount compared to a traditional mortgage. This can enable homebuyers to purchase a more expensive property or have extra funds for other purposes.

- Flexibility: Interest-only mortgages can provide borrowers with more financial flexibility, especially during the interest-only period. This can be valuable for individuals with fluctuating incomes or those who anticipate increased income in the future.

Considerations and Potential Drawbacks

While interest-only mortgages offer advantages, it’s crucial to understand the potential drawbacks and consider whether this type of loan aligns with your financial goals and circumstances. Here are some important factors to consider:

- Higher Long-Term Costs: Although the initial payments are lower, it’s important to recognize that interest-only mortgages can result in higher total interest costs over the life of the loan. This is because the principal balance remains unchanged during the interest-only period, causing the overall cost of borrowing to be higher compared to a traditional mortgage.

- Payment Shock: When the interest-only period ends, and the loan transitions to requiring both principal and interest payments, borrowers may experience a significant increase in monthly payments. This shift can be challenging for individuals who have not adequately prepared for the change in budget.

- Property Value Fluctuations: With an interest-only mortgage, there is a risk associated with the potential decline in the value of the property. If the property value decreases, borrowers may find themselves owing more than the property is worth, which can pose challenges if they need to sell or refinance.

- Qualification Criteria: Lenders often have stricter qualification requirements for interest-only mortgages. Borrowers typically need stronger credit scores, larger down payments, and stable income to be eligible for this type of loan.

- Limited Availability: Interest-only mortgages may not be widely available from all lenders. Therefore, it’s essential to research and compare different lenders to find the ones that offer this type of loan and determine the associated terms and conditions.

Who Should Consider an Interest-Only Mortgage Loan?

An interest-only mortgage loan is not suitable for everyone, but it can be a viable option for certain individuals based on their financial situation and goals. Here are some scenarios where an interest-only mortgage loan may be worth considering:

- Short-Term Ownership: If you plan to sell the property before the interest-only period ends, an interest-only mortgage can be advantageous as you can benefit from lower payments during your ownership.

- Investment Strategy: If you have a well-thought-out investment strategy in place and are confident in generating higher returns by investing the extra funds elsewhere, an interest-only mortgage can provide you with the necessary flexibility.

- Temporary Income Reduction: If you anticipate a decrease in income temporarily, such as starting a business or taking a sabbatical, an interest-only mortgage can help you manage your cash flow during that period.

Interest-only mortgage loans can offer certain advantages, such as lower initial payments and increased financial flexibility. However, it’s essential to carefully evaluate the potential drawbacks, including higher long-term costs and the possibility of payment shock. Consider your financial goals, circumstances, and risk tolerance before deciding whether an interest-only mortgage loan is the right choice for you.

What Is an Interest-only Mortgage? | LowerMyBills

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What is an interest-only mortgage loan?

An interest-only mortgage loan is a type of loan where the borrower pays only the interest on the loan for a specific period of time, usually for the initial years. This means that the monthly payments do not include any principal repayment, resulting in lower monthly payments during the interest-only period.

How does an interest-only mortgage loan work?

During the interest-only period, borrowers can choose to pay only the interest or pay additional amounts towards the principal. Once the interest-only period ends, the borrower is required to pay both the principal and the interest, resulting in higher monthly payments. This period can vary depending on the terms of the loan.

What are the benefits of an interest-only mortgage loan?

Some benefits of an interest-only mortgage loan include lower initial monthly payments, which can be helpful for borrowers who expect their income to increase in the future. It can also provide flexibility for those who plan to sell the property before the principal repayment period begins.

Are there any drawbacks to an interest-only mortgage loan?

Yes, there are drawbacks to an interest-only mortgage loan. The main drawback is that the principal balance does not decrease during the interest-only period, which means that equity in the property does not build up. Additionally, once the interest-only period ends, borrowers may face higher monthly payments, which could become a financial burden if their circumstances change.

Who is eligible for an interest-only mortgage loan?

Eligibility for an interest-only mortgage loan depends on various factors, including the lender’s requirements, the borrower’s creditworthiness, and the loan-to-value ratio. Generally, borrowers with a strong credit history and a high down payment are more likely to qualify for an interest-only mortgage loan.

Can interest-only mortgage loans be refinanced?

Yes, interest-only mortgage loans can be refinanced, depending on the borrower’s financial situation and the lender’s policies. Refinancing can help borrowers extend the interest-only period, adjust the interest rate, or switch to a different type of loan.

What happens after the interest-only period ends?

After the interest-only period ends, borrowers are required to start paying both the principal and the interest. This can significantly increase the monthly payments. It is important for borrowers to plan ahead and consider their financial capabilities for the post-interest-only period.

Are interest-only mortgage loans suitable for everyone?

Interest-only mortgage loans may be suitable for certain individuals, such as those with a stable income, a clear repayment plan, and a good understanding of the risks involved. However, it is essential for borrowers to carefully evaluate their financial situation and consult with a financial advisor or mortgage professional before opting for an interest-only mortgage loan.

Final Thoughts

An interest-only mortgage loan is a type of loan where borrowers are only required to pay the interest for a certain period of time, usually the first few years. This means that the principal amount borrowed remains unchanged during this period. The main advantage of an interest-only mortgage is that it allows borrowers to have lower monthly payments initially. However, it’s important to note that once the interest-only period ends, borrowers will need to start paying both the principal and interest, which can result in higher monthly payments. It’s crucial for borrowers to fully understand the terms and implications of an interest-only mortgage loan before considering it as an option.