Debt refinancing may sound like a complicated financial term, but its benefits can have a significant impact on your financial well-being. In simple terms, debt refinancing refers to replacing an existing loan with a new one, usually at a lower interest rate. This can help you save money by reducing the amount you pay in interest over time. But the benefits don’t stop there. By refinancing your debt, you can also potentially lower your monthly payments, improve your credit score, and gain greater control over your financial future. In this article, we’ll delve deeper into what debt refinancing is and explore the various advantages it brings. So, if you’re looking to improve your financial situation and save money in the long run, keep reading to discover the world of debt refinancing and its benefits.

What is Debt Refinancing and Its Benefits

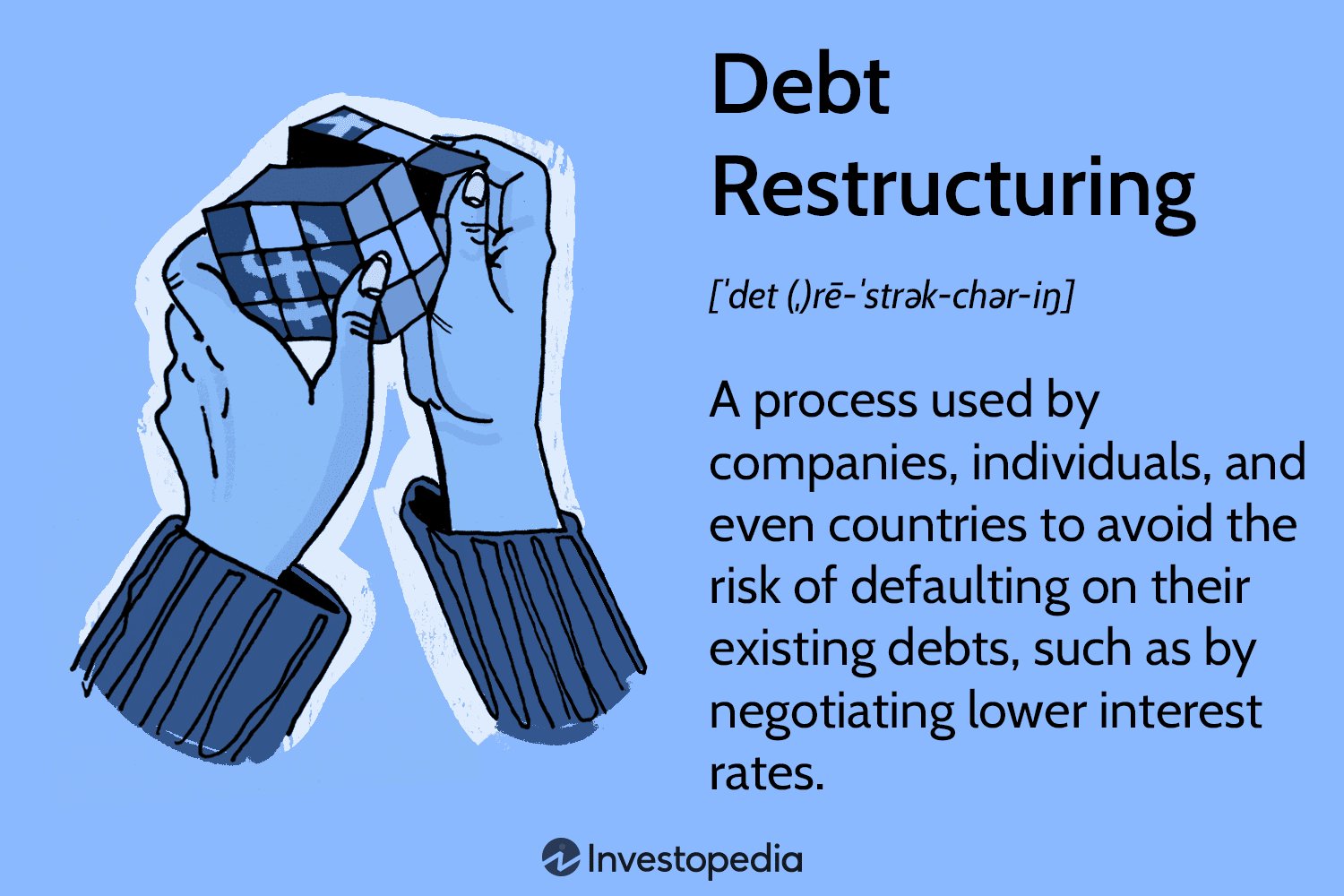

Debt refinancing is a financial strategy that involves replacing an existing loan or debt obligation with a new loan, typically with more favorable terms. It is a powerful tool that individuals and businesses can use to manage their debt, improve their cash flow, and potentially save money in the long run. In this article, we will explore the concept of debt refinancing in detail and examine its benefits.

Understanding Debt Refinancing

Debt refinancing is essentially the process of taking out a new loan to pay off an existing loan. This can be done for various types of debt, including personal loans, mortgages, credit card debt, and business loans. By refinancing, borrowers aim to secure more favorable interest rates, extend the repayment period, or change other terms to better suit their financial needs.

When you refinance your debt, you essentially replace your old debt with a new one. The new loan is used to pay off the original debt, and you then make payments on the new loan according to the agreed-upon terms. Debt refinancing can be done with the same lender or with a different financial institution.

The Benefits of Debt Refinancing

Debt refinancing offers several potential benefits, which can vary depending on individual circumstances. Here are some key advantages that borrowers can gain from debt refinancing:

1. Lower Interest Rates

One of the primary reasons borrowers choose to refinance their debt is to secure a lower interest rate. Interest rates can fluctuate over time, and if you took out a loan when rates were high, refinancing can help you take advantage of lower rates available in the market. By reducing your interest rate, you can save a significant amount of money on interest payments over the life of the loan.

2. Reduced Monthly Payments

Refinancing your debt can also lead to lower monthly payments. By extending the repayment period or securing a lower interest rate, you can reduce the amount you need to pay each month. This can provide immediate relief to your cash flow, allowing you to allocate funds to other essential expenses or financial goals.

3. Consolidating Debt

Another benefit of debt refinancing is the ability to consolidate multiple debts into a single loan. If you have multiple high-interest debts, such as credit card balances or personal loans, consolidating them into one loan can simplify your financial life. Not only will you have a single monthly payment to manage, but you may also be able to secure a lower overall interest rate. This can make it easier to keep track of your debt and potentially save money on interest charges.

4. Improving Credit Score

Debt refinancing can also have a positive impact on your credit score. When you consolidate multiple debts or make timely payments on a refinanced loan, it demonstrates to credit bureaus that you are managing your debt responsibly. This can help improve your credit score over time, making it easier for you to qualify for future loans or credit opportunities at more favorable rates.

5. Changing Loan Terms

In addition to lowering interest rates and reducing monthly payments, debt refinancing also allows borrowers to modify other loan terms. For example, you can choose to switch from an adjustable-rate mortgage to a fixed-rate mortgage, providing stability and predictability in your monthly payments. Similarly, you may be able to modify the repayment period, allowing you to pay off the debt sooner or extend it to reduce monthly obligations further.

6. Accessing Equity

For homeowners, debt refinancing can be an avenue to access the equity built up in their property. By opting for a cash-out refinance, borrowers can refinance their mortgage for an amount greater than the outstanding balance and receive the excess funds as a lump sum. This can be useful for financing home renovations, consolidating high-interest debt, or investing in other opportunities.

7. Reduced Stress and Improved Financial Management

Managing multiple debts with different interest rates and due dates can be stressful and confusing. By refinancing and consolidating your debt, you streamline your finances and simplify your monthly payments. This can provide peace of mind, reduce financial stress, and offer improved financial management.

Debt refinancing is a powerful financial strategy that can help individuals and businesses improve their financial well-being. By securing lower interest rates, reducing monthly payments, consolidating debt, and modifying loan terms, borrowers can better manage their debt and potentially save money in the long run. It is essential to carefully consider the costs and benefits of refinancing and consult with financial professionals to make informed decisions. Remember, debt refinancing is not a one-size-fits-all solution, and its suitability depends on individual circumstances.

What is debt refinancing?

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What is debt refinancing and how does it work?

Debt refinancing refers to the process of replacing an existing debt obligation with a new one that has more favorable terms. It involves taking out a new loan to pay off the existing debt, usually at a lower interest rate or with extended repayment terms. This can help borrowers to save money on interest payments and manage their debt more effectively.

What are the benefits of debt refinancing?

Debt refinancing can offer several benefits, including:

1. Can debt refinancing help reduce monthly payments?

Yes, debt refinancing can potentially lower your monthly payments. By securing a loan with a lower interest rate or longer repayment period, you can spread out your debt over a longer period, resulting in reduced monthly payment obligations.

2. Can debt refinancing save money on interest payments?

Absolutely. If you are able to secure a new loan with a lower interest rate than your current debt, you can save money on interest payments over the life of the loan. This can lead to substantial long-term savings.

3. Is it possible to consolidate multiple debts through refinancing?

Yes, debt refinancing can be used to consolidate multiple debts into a single loan. This simplifies your repayment process, reduces the number of monthly payments, and may offer better interest rates or terms.

4. Can debt refinancing improve credit scores?

In some cases, debt refinancing can positively impact credit scores. When you successfully make payments on your refinanced loan, it demonstrates a responsible approach to debt management, which can improve your creditworthiness over time.

5. Are there any risks associated with debt refinancing?

While debt refinancing can be beneficial, it’s important to consider potential risks. These may include transaction fees, prepayment penalties on existing debt, and the possibility of ending up with a higher interest rate if market conditions change unfavorably.

6. Is debt refinancing suitable for all types of debt?

Debt refinancing can be useful for various types of debt, such as credit card debt, personal loans, student loans, or even mortgages. However, it’s essential to evaluate the terms and conditions of the new loan to ensure it aligns with your financial goals.

7. How can I determine if debt refinancing is right for me?

Deciding whether debt refinancing is suitable for you depends on factors such as your current interest rate, outstanding debt balance, credit score, and financial goals. Consulting with a financial advisor or using online calculators can help you assess the potential benefits and costs.

8. How long does the debt refinancing process usually take?

The time required for the debt refinancing process varies depending on factors such as the complexity of the loan, lender requirements, and the efficiency of your documentation. On average, it can take anywhere from a few weeks to a couple of months to complete the process.

Final Thoughts

Debt refinancing involves replacing existing debts with a new loan that offers more favorable terms. This process can help borrowers consolidate their debts, reduce interest rates, and lower their monthly payments. By refinancing, individuals and businesses have the opportunity to regain control of their finances and improve their overall financial situation. Debt refinancing enables them to manage their debts more efficiently and effectively, ultimately leading to financial stability and peace of mind. Overall, debt refinancing offers numerous benefits including reduced interest costs, improved cash flow, simplified debt management, and the potential to pay off debts sooner. It is a smart strategy for anyone looking to improve their financial well-being.