The prime rate in lending is an important concept that impacts borrowers and lenders alike. Put simply, it is the interest rate that banks charge their most creditworthy customers. But this seemingly straightforward term holds significant implications, affecting everything from mortgage rates to credit card APRs. So, what is the prime rate in lending, and why does it matter? In this article, we’ll dive into the details, exploring how the prime rate works and how it can shape the lending landscape for individuals and businesses. Get ready to unravel the mysteries of the prime rate and gain a deeper understanding of its impact. Let’s begin our journey!

What is the Prime Rate in Lending?

When it comes to borrowing money, understanding how interest rates work is essential. One critical concept in lending is the prime rate. The prime rate serves as a foundation for interest rates across various financial products, including loans and credit cards. In this article, we will delve into what the prime rate is, how it is determined, and the impact it can have on borrowing costs. So, let’s explore the world of prime rates in lending!

Defining the Prime Rate

The prime rate refers to the interest rate that banks and other financial institutions offer to their most creditworthy customers. It serves as a benchmark for setting interest rates on different lending products. Typically, the prime rate is tied to the federal funds rate, which is the interest rate at which banks lend to one another overnight. However, it is important to note that the prime rate is not directly determined by the Federal Reserve.

Financial institutions set their own prime rates, which are influenced by various factors such as the federal funds rate, overall economic conditions, and the institution’s cost of borrowing. The prime rate is often presented as a percentage above or below the federal funds rate.

Factors Influencing the Prime Rate

Several key factors influence the determination of the prime rate. Understanding these factors can help borrowers anticipate potential changes in the prime rate and make informed decisions about their borrowing needs. Here are some of the main factors that financial institutions consider:

- Economic conditions: The state of the economy, including factors like inflation, unemployment rates, and GDP growth, plays a crucial role in setting the prime rate. When the economy is thriving, the prime rate tends to be higher, reflecting increased borrowing costs. Conversely, during economic downturns, financial institutions may lower the prime rate to stimulate borrowing and economic activity.

- Federal Reserve policy: Although the Federal Reserve does not directly set the prime rate, its monetary policy decisions can indirectly impact the prime rate. When the Federal Reserve raises or lowers the federal funds rate, it affects short-term borrowing costs for banks. Financial institutions adjust their prime rates accordingly to align with market conditions.

- Risk assessment: Financial institutions consider the creditworthiness of their customers when determining the prime rate. Borrowers with higher credit scores and lower default risk may receive more favorable interest rates. This is because lenders view them as less likely to default on their loans, reducing the risk associated with lending to them.

- Competition: The prime rate can also be influenced by competition among financial institutions. If one bank lowers its prime rate to attract more customers, other banks may follow suit to remain competitive in the market. Conversely, if a bank increases its prime rate, others might do the same to maintain profitability.

The Impact of the Prime Rate

The prime rate has a significant impact on the borrowing costs for individuals and businesses. Here’s how the prime rate can affect different types of loans and financial products:

Mortgages:

The prime rate indirectly affects mortgage interest rates. Most mortgages have rates that are based on a certain percentage above the prime rate. For example, if the prime rate is 4% and a mortgage has an interest rate of prime rate + 1%, the borrower would pay an interest rate of 5%. Therefore, changes in the prime rate can impact the affordability of mortgages and monthly mortgage payments.

Personal Loans and Auto Loans:

Similar to mortgages, personal loans and auto loans often have interest rates tied to the prime rate. Borrowers with excellent credit scores may qualify for loan rates below the prime rate, while those with lower credit scores may face rates above the prime rate. Therefore, changes in the prime rate can directly affect the interest rates on these types of loans.

Credit Cards:

Many credit cards have variable interest rates that are directly tied to the prime rate. If the prime rate increases, credit card interest rates also rise, increasing the cost of carrying a balance. On the other hand, a decrease in the prime rate can lead to lower credit card interest rates, providing potential savings for cardholders.

Business Loans:

Business loans, including lines of credit and term loans, often have interest rates based on the prime rate. Small businesses with strong credit profiles may qualify for rates below the prime rate, while riskier businesses might face higher rates. Changes in the prime rate can have a direct impact on the cost of borrowing for businesses.

Monitoring the Prime Rate

Given the significance of the prime rate on borrowing costs, it is important for individuals and businesses to monitor any changes or potential shifts in the prime rate. There are several ways to stay informed:

- Financial news and websites: Keeping up with financial news and visiting reputable websites can provide valuable insights into changes in the prime rate. Many financial news outlets regularly report on interest rate movements and the factors influencing them.

- Bank and lender updates: Financial institutions may notify their customers of any changes in their prime rates. Subscribing to newsletters or email updates from your bank or lender can help you stay informed about adjustments in interest rates.

- Financial advisors: Seeking guidance from financial advisors can be beneficial, especially when planning major borrowing decisions. Advisors can provide personalized insights based on your financial situation and help you navigate the impact of prime rate changes.

The prime rate serves as a crucial benchmark for interest rates in lending. Financial institutions determine their prime rates based on factors such as economic conditions, Federal Reserve policy, risk assessment, and competition. The prime rate influences the borrowing costs for various financial products, including mortgages, personal loans, credit cards, and business loans. Monitoring changes in the prime rate is important for borrowers to anticipate potential shifts in interest rates and make informed borrowing decisions.

Prime Rate 101: A Quick and Simple Explanation in Just 1 Minute

Frequently Asked Questions

Frequently Asked Questions (FAQs)

What is the prime rate in lending?

The prime rate in lending refers to the interest rate that banks charge their most creditworthy customers. It serves as a benchmark for the interest rates offered on various types of loans, such as mortgages, personal loans, and business loans.

How is the prime rate determined?

The prime rate is typically determined by the federal funds rate set by the central bank, which influences the interest rates at which banks lend to each other. However, individual banks may also consider their cost of funds, market conditions, and risk factors when setting their prime rates.

Does the prime rate fluctuate?

Yes, the prime rate can fluctuate over time. It often changes in response to adjustments made by the central bank to the federal funds rate. Economic factors, such as inflation, economic growth, and market conditions, can also influence changes in the prime rate.

Who benefits from a low prime rate?

A low prime rate benefits borrowers as it usually leads to lower interest rates on loans. Individuals and businesses seeking credit can take advantage of the lower borrowing costs associated with a low prime rate.

Can the prime rate affect my mortgage interest rate?

Yes, the prime rate can have an impact on mortgage interest rates. Many adjustable-rate mortgages are tied to the prime rate, meaning changes in the prime rate can result in changes to the interest rate and monthly mortgage payments.

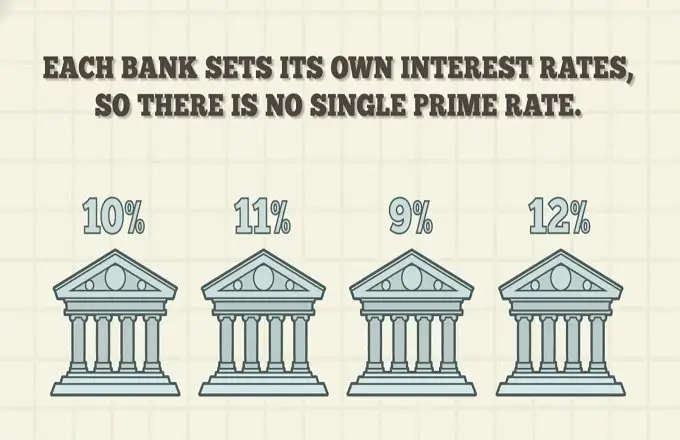

Is the prime rate the same for all banks?

No, the prime rate can differ slightly among banks. While most banks base their prime rate on the federal funds rate, they may incorporate additional factors or adjust the rate based on their own business strategies, cost of funds, and market conditions.

What credit score is needed to qualify for the prime rate?

To qualify for the prime rate, borrowers generally need an excellent credit score. A credit score above 700 is typically considered favorable for obtaining the most favorable interest rates, including the prime rate.

How often does the prime rate change?

The prime rate can change periodically, although it is often adjusted in response to significant changes in the federal funds rate. Changes in the prime rate are typically announced by individual banks and are not standardized across all financial institutions.

Final Thoughts

The prime rate in lending refers to the interest rate that commercial banks charge their most creditworthy customers. It serves as a benchmark for various loan products, including mortgages, personal loans, and business loans. This rate is determined by the central bank of a country and is influenced by factors such as economic conditions, inflation, and monetary policies. Lenders often set their interest rates based on the prime rate, adding a certain percentage to it. Borrowers with a good credit history can benefit from lower interest rates, while those with a less favorable credit profile may face higher rates. Understanding the prime rate in lending is essential for borrowers and enables them to make informed decisions when seeking credit.